Bralorne case study in media this week.

See coverage in the

Canadian Mining Journal

Mining.com

Welcome.ai

Geomechanics.io

indebox.io

of the

Bralorne Gold case study

published last week.

Really insightful editorials around the value that Stormlands offers.

Stormlands Mining publishes independent case study on Bralorne Gold Project

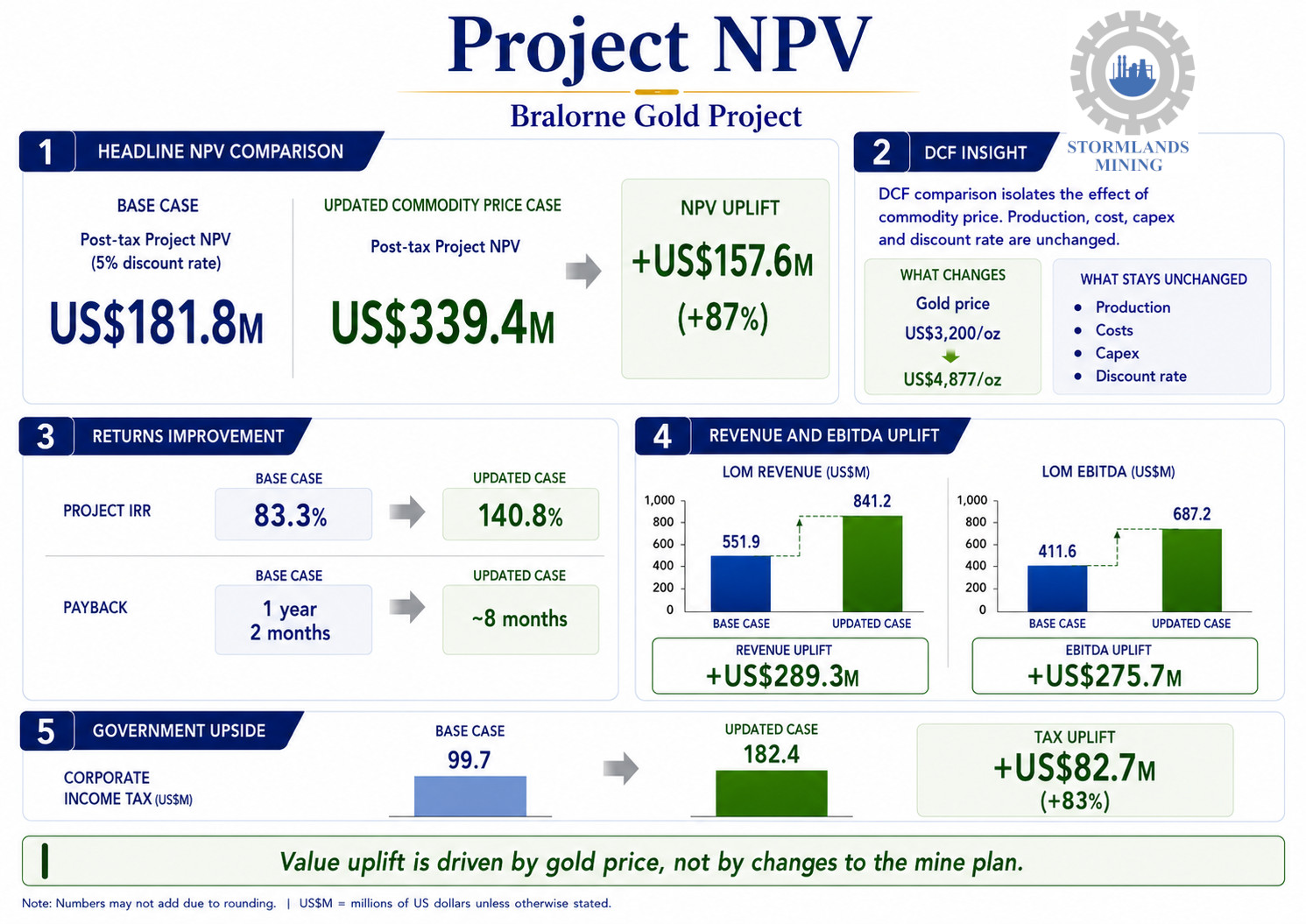

READ FULL CASE STUDY HERE. Stormlands Mining has published a new independent case study on the Bralorne Gold Project in British Columbia, Canada. Using data extracted from the NI 43-101 Technical Report on the Mineral Resource Estimate dated June 26 2026, Stormlands developed an illustrative economic model that generates a post-tax project Net Present Value (NPV) of US$181.8 million at a 5% discount rate, with a post-tax project Internal Rate of Return (IRR) of 83.3% and a payback period of 1 year and 2 months.

The model also generates:

- Life-of-mine revenue of US$551.9 million

- Life-of-mine EBITDA of US$411.6 million

- Life-of-mine post-tax free cash flow of US$232.6 million

- Life-of-mine corporate income tax of US$99.7 million

- Life-of-mine commercial royalties of US$25.9 million

- Mine life of 5.37 years

Updated Commodity Prices

Stormlands then updated the model using a updated gold price to the average of March 2026, while holding all other core assumptions constant, including mine life, production schedule, recoveries, operating costs, capital costs, sustaining capital, royalties, fiscal assumptions and discount rate.

Under this scenario, the gold price increases from US$3,200/oz to US$4,877/oz. Project NPV increases from US$181.8 million to US$339.4 million, representing an uplift of approximately US$157.6 million, or 87%, compared with the base case.

Project IRR increases from 83.3% to 140.8%, while payback improves from 1 year and 2 months to approximately 8 months.

Life-of-mine revenue increases from US$551.9 million to US$841.2 million. Life-of-mine EBITDA increases from US$411.6 million to US$687.2 million, while life-of-mine post-tax free cash flow increases from US$232.6 million to US$425.6 million.

The underlying resource base, mine life, production profile, capital costs and operating costs remain unchanged between the two scenarios.

The uplift is therefore driven entirely by the updated gold price.

Roisin O’Connell, CEO of Stormlands Mining, said: “The mining industry has a valuation problem. Billions of dollars are invested in exploration long before a PEA exists, yet investors are expected to value projects using little more than drill results, presentations and intuition. We believe that approach belongs to another era.

AI and analytics now make it possible to create transparent, structured economic models directly from technical report data, moving valuation years earlier in the asset lifecycle. That doesn’t replace formal engineering studies, it complements them. It gives the market a way to connect geology to economics, exploration to value, and technical disclosure to investment decisions while projects are still being shaped.”

Margin expansion

The discounted cash flow comparison shows that stronger gold prices materially improve project margins.

Life-of-mine EBITDA increases from US$411.6 million to US$687.2 million.

Net smelter return increases from US$851.66/t ore to US$1,298.09/t ore. Cash operating margin increases from US$694.13/t ore to US$1,140.56/t ore, while operating margin percentage increases from 81.5% to 87.9%.

This means that the same physical mine plan generates substantially higher profitability without any change to mining, processing, capital or operating cost assumptions.

Value drivers

Stormlands’ sensitivity analysis shows that gold price is overwhelmingly the dominant driver of project value.

In the base case model, the Project NPV is approximately US$181.8 million. Sensitising price moves NPV from approximately US$152 million to US$212 million.

By comparison, operating cost sensitivity moves NPV from approximately US$176 million to US$188 million. Capital cost sensitivity moves NPV from approximately US$177 million to US$186 million, while discount-rate sensitivity produces a similar range.

The general Price Factor and Gold Price Factor produce the same valuation movement, confirming that Bralorne behaves economically as a gold project.

Operating cost is important, but it is not the dominant value driver. Capital cost sensitivity is relatively limited, reflecting the strength of the project’s modelled margins and the short, front-loaded mine life.

Heatmap analysis

The price and operating cost heatmap, modelling 20% increases and decreases in gold price and operating cost, provides one of the strongest insights from the Bralorne case study.

Under the base case model, Project NPV is approximately US$182 million at 100% gold price and 100% operating cost.

In the downside scenario of 20% lower gold price and 20% higher operating cost, Project NPV remains positive at approximately US$109 million.

In the upside scenario of 20% higher gold price and 20% lower operating cost, Project NPV increases to approximately US$254 million.

The heatmap demonstrates that the project remains positive across all tested scenarios. It also shows that gold price has substantially greater influence on valuation than operating costs.

One notable insight is that a 10% increase in gold price more than offsets a 20% increase in operating cost. At 110% gold price and 120% operating cost, Project NPV is approximately US$200 million, still above the base case.

Economic resilience

One of the most important findings from the case study is the project’s modelled resilience.

Even under scenarios combining lower gold prices and higher operating costs, the model continues to generate positive value.

This suggests that the project’s illustrative economics are supported by the combination of high grade, strong net smelter return per tonne, strong operating margins and a short payback profile.

The Bralorne Gold Project is owned by Talisker Resources Ltd. Stormlands modelled the project using public technical disclosure and independent analysis.

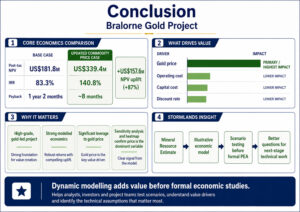

Stormlands Mining publishes independent case study on Illinois Creek Gold Project – Illustrative scenario establishes project NPV of US$226.2m and shows current commodity prices nearly double NPV to US$448.6 million

Stormlands Mining has published a new independent case study on the Illinois Creek Project in western Alaska, USA. Using data extracted from the NI 43-101 Technical Report effective data January 2026, the Stormlands model generates an post-tax project Net Present Value (NPV) of US$226.2 million at an 8% discount rate, with a post-tax project Internal Rate of Return (IRR) of 36.8% and a payback period of 2 years and 7 months.

The model also generates:

-

- Life-of-mine revenue of US$1.15 billion

- Life-of-mine EBITDA of US$805 million

- Life-of-mine corporate income tax of US$190 million

- Mine life of 10.27 years

- Initial capital requirement of US$150 million

Stormlands then updated the model using March 2026 commodity prices while holding the core physical and cost assumptions constant, including mine life, production output, capital costs, operating costs and discount rate.

Under this updated commodity price scenario, modelled post-tax project NPV increases from US$226.2 million to US$448.6 million, representing an uplift of approximately US$222 million, or 98%.

Project IRR increases from 36.8% to 61.4%, while payback improves from 2 years and 7 months to 1 year and 7 months.

Life-of-mine revenue increases from US$1.15 billion to US$1.69 billion. Life-of-mine EBITDA increases from US$805 million to US$1.32 billion. Modelled life-of-mine corporate income tax increases from US$190 million to US$345 million, while modelled government royalties increase from US$34.6 million to US$50.6 million.

The underlying resource, mine life, capital cost, operating cost and discount rate remain unchanged between the two scenarios. The uplift is driven by the commodity price environment.

Value drivers

- Stormlands’ sensitivity analysis shows that the overall commodity price factor is the strongest value driver in the Illinois Creek model.

- In the NI 43-101-derived base case, a 10% increase or decrease in the overall commodity price factor moves project NPV from US$178 million to US$274 million. In the updated commodity price model, the same sensitivity moves project NPV from US$378 million to US$519 million.

- Gold is the dominant individual metal price driver. In the NI 43-101-derived model, a 10% increase or decrease in gold price moves project NPV from US$190 million to US$262 million. In the updated commodity price model, the same gold price sensitivity moves project NPV from US$398 million to US$499 million.

- Silver is a meaningful secondary driver, and its contribution increases under the updated commodity price case. In the updated model, a 10% increase or decrease in silver price moves project NPV from US$429 million to US$469 million.

- Operating cost and capital cost remain important, but the model shows that Illinois Creek’s valuation is more sensitive to commodity prices than to cost variation within the tested ranges.

Gold-led project with meaningful silver leverage

- The Stormlands model shows Illinois Creek as a gold-led project, with silver providing a meaningful secondary contribution.

- In the NI 43-101-derived base case, gold contributes approximately US$867 million of payable revenue, while silver contributes approximately US$286 million. In the updated commodity price case, gold revenue increases to approximately US$1.21 billion, while silver revenue increases to approximately US$478 million.

- The revenue mix shifts from approximately 75% gold and 25% silver in the base case to approximately 72% gold and 28% silver in the updated commodity price case. Gold remains the dominant revenue driver, but silver becomes more important under the updated price deck.

The Illinois Creek model forms part of the Stormlands Mining Library, a growing repository of mining asset valuation models built from public technical reports and company disclosures.

The case study demonstrates how a technical report with no published economic analysis can be converted into an scenario-driven valuation model. It allows users to ask practical economic questions before a formal PEA is available in order to understand the value drivers that influence the project economics.

Using data extracted from the NI 43-101 Technical Report effective date 30 November 2025 for the Regnault Deposit, Stormlands developed an illustrative economic model generating a post-tax project Net Present Value (NPV) of US$983.2 million at a 5% discount rate, with a post-tax Internal Rate of Return (IRR) of 35% and a payback period of 2 years and 10 months.

Illustrative scenario shows how Frotet Gold Project economics may respond to March 2026 commodity prices

Dublin, Ireland — [29 June 2026] — Stormlands Mining has published a new case study on the Frotet Project’s Regnault Deposit in Québec, Canada, demonstrating how a publicly available NI 43-101 Technical Report can be converted into a dynamic economic valuation model, even in the absence of an Economic Assessment.

Using data extracted from the NI 43-101 Technical Report effective date 30 November 2025 for the Regnault Deposit, Stormlands developed an illustrative economic model based on the published mineral resource, metallurgical information and technical disclosure.

The Stormlands base case model generates a post-tax project Net Present Value (NPV) of US$983.2 million at a 5% discount rate, with a post-tax Internal Rate of Return (IRR) of 35% and a payback period of 2 years and 10 months.

The model also generates:

- Life-of-mine revenue of US$6.0 billion

- Life-of-mine EBITDA of US$3.47 billion

- Life-of-mine post-tax free cash flow of US$1.87 billion

- Initial capital requirement of US$300 million

Stormlands then updated the model using March 2026 commodity prices while holding all other core assumptions constant, including mine life, production schedule, recoveries, operating costs, capital costs and fiscal assumptions.

Under this updated commodity price scenario, project NPV increases to US$3.08 billion, representing an increase of US$2.10 billion, or 213%, compared with the base case.

Project IRR increases from 34.8% to 92.6%, while payback improves from 2 years and 10 months to 1 year and 1 month.

Life-of-mine revenue increases from US$6.0 billion to US$11.8 billion. Life-of-mine EBITDA increases from US$3.47 billion to US$8.99 billion, while life-of-mine free cash flow increases from US$1.87 billion to US$5.46 billion.

The underlying resource, mine life, production profile, capital costs and operating costs remain unchanged between the two scenarios.

The uplift is therefore driven entirely by commodity prices.

Margin Expansion

- The discounted cash flow comparison shows that stronger commodity prices materially improve project margins.

- Life-of-mine EBITDA increases from US$3.47 billion to US$8.99 billion.

- Operating margin increases from US$256 per tonne to US$652 per tonne, while operating margin percentage increases from 61.7% to 80.4%.

- This means that the same physical mine plan generates substantially higher profitability without any change to mining or processing assumptions.

Value Drivers

- Stormlands’ sensitivity analysis shows that gold price is overwhelmingly the dominant driver of project value.

- In the base case model, 10% fluctuation in gold price pushes the project NPV range to US$766 million and US$1.20 billion.

- In the updated commodity price model, 10% fluctuation in gold price pushes the project NPV range to US$2.66 billion and US$3.50 billion.

- The overall commodity price factor produces almost identical results, confirming that the project behaves economically as a gold project.

- Operating cost is the second most important value driver, while discount rate has a moderate influence on valuation.

- Capital cost sensitivity is relatively limited, reflecting the project’s strong margins and moderate initial capital requirement.

- Silver contributes additional revenue but has minimal influence on overall valuation, confirming that the investment case is overwhelmingly driven by gold.

Heatmap Analysis

- The price and operating cost heatmap, modelling 20% increase and decrease in price and operating cost, provides one of the strongest insights from the Frotet case study.

- Under the base case model, NPV ranges from US$370 million in the downside scenario of 20% lower commodity prices and 20% higher operating costs. A 20% increase in commodity prices and decrease in operating costs push the base case NPV to US$1.60 billion.

- The heatmap demonstrates that the project remains positive across all tested scenarios.

- It also shows that commodity prices have substantially greater influence on valuation than operating costs.

- Importantly, the updated commodity price scenario does not simply improve the base case. It shifts the entire valuation range upward.

- Even the most conservative scenario in the updated commodity price heatmap generates a higher valuation than many development-stage gold projects achieve under base case assumptions.

Economic Resilience

- One of the most important findings from the case study is the project’s resilience.

- Even under scenarios combining lower commodity prices and higher operating costs, the model continues to generate substantial positive value.

- This suggests that the project’s economics are supported not only by commodity prices but also by the combination of high grades, strong margins and moderate capital intensity.

The Frotet model forms part of the Stormlands Mining Library, a growing repository of mining asset valuation models built from public technical reports and company disclosures.

The Library is designed to help investors, mining companies, banks, advisers and other stakeholders understand the key drivers of mining asset economics.

The Frotet Project is owned by Sumitomo Metal Mining Canada Ltd. and Kenorland Minerals Ltd. Stormlands modelled the project using public technical disclosure and independent analysis.

Stormlands Mining publishes Sandman Gold Project case study showing modelled NPV increasing to US$667 million under updated commodity price assumptions

Click here to view the full case study

Dublin, Ireland — 22 June 2026 — Stormlands Mining has published a new case study on the Sandman Gold Project in Humboldt County, Nevada, USA, including an illustrative updated commodity price scenario which increases modelled project NPV from approximately US$210.5 million to approximately US$667.4 million.

Using the mine plan and economic data contained in the NI 43-101 Preliminary Economic Assessment for the Sandman Gold Project, with an effective date of 5 January 2026, Stormlands rebuilt a base case financial model for Sandman using gold and silver price inputs from the NI 43-101 of US$2,600/oz gold and US$20/oz silver.

On this basis, the Stormlands model generated a post-tax project Net Present Value (NPV) of approximately US$210.5 million at a 6% discount rate, with a project IRR of approximately 101.2% and payback of approximately 1 year and 2 months.

Stormlands then updated the same model using updated commodity price assumptions of US$4,877.40/oz gold and US$74.92/oz silver. All other core assumptions were held constant, including mine life, ore processed, gold grade, silver grade, recoveries, production profile, operating cost, capital cost, sustaining capital and fiscal assumptions.

Under this updated commodity price scenario, modelled project NPV increased to approximately US$667.4 million.

This represents an uplift of approximately US$456.9 million, or approximately 217%, compared with the NI 43-101 extracted base case model.

Life-of-mine revenue increased from approximately US$900.4 million in the base case to approximately US$1.72 billion under the updated commodity price scenario. Life-of-mine EBITDA increased from approximately US$440.7 million to approximately US$1.24 billion. Post-tax project free cash flow increased from approximately US$303.2 million to approximately US$937.4 million.

The modelled payback period improved from approximately 1 year and 2 months to approximately 5 months.

The Sandman case study highlights the project’s strong leverage to gold price. Revenue increases by approximately 91% under the updated commodity price scenario, while post-tax NPV increases by approximately 217%. This demonstrates the operational gearing of the project, with a substantial portion of additional commodity revenue flowing through to EBITDA, free cash flow and NPV.

Róisín O’Connell, CEO of Stormlands Mining, said:

“Sandman is a clear example of why mining needs to move beyond static reports and spreadsheets. The technical documents provides the foundation, but the real value comes when that information is converted into structured, comparable and updateable data.

“The mining sector talks a lot about AI, but not enough about the data standards underpin the industry. The industry needs a common data layer that makes technical and economic information discoverable, structured, governed and comparable. Stormlands has built a scalable data foundation so that project economics can be updated, tested, compared and understood in real time.

“In the Sandman case study, we have kept the mine plan, ore processed, grades, recoveries, operating costs, capital costs, sustaining capital and fiscal assumptions unchanged. We have only updated the commodity price assumptions. That single change increases modelled project NPV from approximately US$210 million to approximately US$667 million.

“The broader point is not simply that higher gold and silver prices increase valuation. It is that once technical disclosure has been structured into a dynamic model, users can immediately see how the project behaves under different market conditions. They can test gold price, silver price, operating cost, capital cost, discount rate, royalties, taxes and production assumptions, and understand which variables really drive value.”

Margin expansion

The revenue report shows net smelter return increasing from approximately US$46.37/t ore in the NI 43-101 extracted case to approximately US$88.73/t ore in the updated commodity price case.

Operating cost remains unchanged at approximately US$22.51/t ore.

As a result, cash operating margin increases from approximately US$23.86/t ore to approximately US$66.22/t ore. Operating margin percentage increases from approximately 51.5% to approximately 74.6%.

This means that, under the updated commodity price assumptions, the same physical mine plan generates materially higher margin per tonne processed.

Value drivers

Stormlands’ sensitivity analysis shows that gold price is the dominant value driver for Sandman.

In the NI 43-101 extracted base case, the price factor sensitivity range is approximately US$160 million to US$261 million NPV. The gold price factor sensitivity range is approximately US$161 million to US$260 million NPV.

In the updated commodity price case, the price factor sensitivity range is approximately US$571 million to US$763 million NPV. The gold price factor sensitivity range is approximately US$575 million to US$760 million NPV.

The close alignment between the price factor and gold price factor confirms that Sandman is overwhelmingly a gold-driven project. Gold accounts for approximately 98% of revenue in the NI 43-101 extracted case and approximately 96% of revenue in the updated commodity price case.

Silver provides useful by-product support, but it does not drive the investment case. Silver revenue increases from approximately US$16.5 million in the base case to approximately US$61.8 million in the updated commodity price case, helping reduce AISC from approximately US$1,472.70/oz gold to approximately US$1,397.76/oz gold.

Operating cost is the second most important value driver. However, the updated commodity price case materially reduces the relative impact of operating cost inflation. In the NI 43-101 extracted model, operating cost sensitivity ranges from approximately US$186 million to US$235 million NPV. In the updated commodity price model, operating cost sensitivity ranges from approximately US$643 million to US$692 million NPV.

Capital cost sensitivity is limited in both scenarios, reflecting Sandman’s relatively low initial capital requirement of approximately US$36.25 million compared with its modelled cash-flow potential.

Heatmap analysis

The price and operating cost heatmap provides one of the strongest findings in the Sandman case study.

In the NI 43-101 extracted model, the base case NPV is approximately US$210 million. Across the heatmap, NPV ranges from approximately US$60.6 million in the downside case of 80% price and 120% operating cost to approximately US$360 million in the upside case of 120% price and 80% operating cost.

In the updated commodity price model, the base case NPV is approximately US$667 million. Across the heatmap, NPV ranges from approximately US$426 million in the downside case of 80% price and 120% operating cost to approximately US$908 million in the upside case of 120% price and 80% operating cost.

This means there is no overlap between the NI 43-101 extracted heatmap valuation range and the updated commodity price heatmap valuation range. The lowest NPV scenario in the updated commodity price heatmap is higher than the highest NPV scenario in the NI 43-101 extracted heatmap.

The updated commodity price case does not simply improve the base case. It shifts the entire valuation range upward.

Government revenues

The Sandman case study also shows that updated commodity prices materially increase projected government revenues.

Government royalties and corporate income tax increase from approximately US$91.4 million in the NI 43-101 extracted base case to approximately US$269.9 million in the updated commodity price case.

This demonstrates that higher commodity prices can materially increase both project-level returns and fiscal contribution.

Moving beyond static technical reports

Stormlands’ analysis highlights the importance of moving beyond static technical report numbers. Public technical reports contain the data required to build robust economic models, but those models need to be structured, updateable and comparable if they are to support better decision-making.

The Sandman model is part of the Stormlands Mining Library, a growing repository of dynamic mining valuation models built from public technical reports and company disclosures. The Library is designed to help users analyse, update and compare mining projects across jurisdictions, commodities and development stages.

The Sandman Gold Project is owned by Borealis Mining Company Limited through Sandman Resources Inc. Stormlands modelled the project using public technical disclosure and independent analysis

Important Notice

This publication has been prepared by Stormlands Mining Ltd. for informational, educational and illustrative purposes only. It is based on publicly available information, including the NI 43-101 Preliminary Economic Assessment of the Sandman Gold Project, Nevada, USA, with an effective date of 5 January 2026, together with independent modelling undertaken by Stormlands Mining.

Stormlands Mining has not been engaged by the project owner or its affiliates to prepare this analysis. This publication has not been reviewed, approved or endorsed by the project owner, its advisers, or any Qualified Person associated with the project.

The analysis presented is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, technical report, mineral resource estimate, mineral reserve estimate, valuation opinion, fairness opinion, investment research report, securities recommendation, offer to sell, solicitation to buy, or investment advice.

Stormlands Mining is not acting as a broker, dealer, investment adviser, corporate finance adviser, Qualified Person, or securities research provider in connection with this publication.

All model outputs are scenario-based and depend on the assumptions used, including commodity prices, exchange rates, discount rates, capital costs, operating costs, taxes, royalties, production schedules, payability, recoveries, treatment and refining charges, timing assumptions and other inputs. Actual results may differ materially from the scenarios presented. Commodity prices, costs, financing conditions, permitting timelines and project development outcomes are uncertain and subject to change.

Stormlands Mining does not represent or warrant that the information or model outputs are complete, accurate or suitable for any particular purpose. Readers should treat this publication as one source of information only and should conduct their own independent technical, financial, legal, tax and investment due diligence before making any decision.

Neither Stormlands Mining nor any of its directors, officers, employees or advisers accepts any liability for any loss arising from reliance on this publication or the information contained in it.

Stormlands Mining publishes Kandiolé Gold Project case study showing modelled NPV increasing to US$1.11 billion under updated gold price assumptions

Click here to read the full case study

Dublin, Ireland — 15 June 2026 — Stormlands Mining has published a new case study on the Kandiolé Gold Project in western Mali, including an illustrative scenario using current commodity prices, which raises the NPV from US$462.1m to US$1.11bn.

Using the mine plan and economic data contained in the NI 43-101 Preliminary Economic Assessment with an effective date of 27 February 2026, Stormlands rebuilt a base case financial model for Kandiolé using a gold price of US$3,100/oz. On this basis, the Stormlands model generated a post-tax project Net Present Value (NPV) of approximately US$462.1 million, with an IRR of 48.9% and payback of approximately 1 year and 9 months.

Stormlands then updated the model using the average of March 2026 gold price: US$4,877.40/oz. All other core assumptions were held constant, including mine life, grade, production profile, operating cost, capital cost, sustaining capital and fiscal assumptions. Under this updated commodity price scenario, modelled project NPV increased to approximately US$1.11 billion.

This represents an uplift of approximately US$648 million, or around 140%, compared with the NI 43-101 base case model.

Life-of-mine revenue increased from approximately US$2.56 billion in the base case to approximately US$4.03 billion under the updated commodity price scenario. Life-of-mine EBITDA increased from approximately US$1.31 billion to approximately US$2.64 billion. The modelled payback period improved from approximately 1 year and 9 months to approximately 1 year.

The Kandiolé case study highlights the project’s strong leverage to gold price. Revenue increases by approximately 57% under the updated commodity price scenario, while post-tax NPV increases by approximately 140%. This demonstrates the operational gearing of the project, with a significant portion of the additional gold revenue flowing through to EBITDA, free cash flow and NPV.

Róisín O’Connell, CEO of Stormlands Mining, said:

“Kandiolé is a powerful example of why mining project valuations need to be dynamic. The technical report provides the foundation, but commodity prices can move quickly and materially change the economic interpretation of a project.

“In this case study, we have kept the mine plan, grade, operating costs, capital costs, sustaining capital and fiscal assumptions unchanged. We have only updated the gold price assumption. That single change increases modelled project NPV from approximately US$462 million to approximately US$1.11 billion.

“The broader point is not simply that higher gold prices increase valuation. It is that once the technical report data has been structured into a dynamic model, users can immediately see how the project behaves under different market conditions. They can test gold price, operating costs, capital costs, discount rate, royalties, taxes and production assumptions, and understand which variables really drive value.

“Kandiolé is particularly interesting because the updated price case does not rely on distant late-life cash flows. A substantial part of the value uplift is generated early in the mine life, improving payback and strengthening the capital recovery profile.”

Net Smelter Return (NSR): The revenue report shows net smelter return increasing from approximately US$82.52/t ore to approximately US$129.88/t ore. Cash operating margin increases from approximately US$50.90/t ore to approximately US$98.26/t ore. This moves Kandiolé from a strong margin asset to a very high margin asset under updated commodity price assumptions.

Value Drivers

Stormlands’ sensitivity analysis shows that gold price is the dominant value driver for Kandiolé. In the NI 43-101 base case, the gold price sensitivity range is approximately US$348 million to US$576 million NPV. In the updated commodity price case, the equivalent range is approximately US$933 million to US$1.29 billion.

Operating cost is the second most important value driver. However, the updated commodity price case materially increases resilience to operating cost inflation. The operating cost sensitivity range is approximately US$416 million to US$508 million in the NI 43-101 base case, compared with approximately US$1.06 billion to US$1.16 billion in the updated commodity price case.

The price and operating cost heatmap provides one of the strongest findings in the case study. In the NI 43-101 base model, the downside scenario of 80% price and 120% operating cost produces an NPV of approximately US$137 million. In the updated commodity price case, the same downside scenario produces an NPV of approximately US$664 million. This is higher than the NI 43-101 base case NPV of approximately US$462 million.

Stormlands’ analysis highlights the importance of moving beyond static technical report numbers. Public technical reports contain the data required to build robust economic models, but those models need to be structured, updateable and comparable if they are to support better decision-making.

The Kandiolé Gold Project is owned by Roscan Gold Corporation. Stormlands modelled the project using the NI 43-101 Preliminary Economic Assessment with an effective date of 27 February 2026.

The Kandiolé model is part of the Stormlands Mining Library, a growing repository of dynamic mining valuation models built from public technical reports and company disclosures. The Library is designed to help users analyse, update and compare mining projects across jurisdictions, commodities and development stages.

Important Notice

This publication has been prepared by Stormlands Mining Ltd. for informational, educational and illustrative purposes only. It is based on publicly available information, including the NI 43-101 Preliminary Economic Assessment of the Kandiolé Project, Mali, West Africa, with an effective date of 27 February 2026, together with independent modelling undertaken by Stormlands Mining.

Stormlands Mining has not been engaged by the project owner or its affiliates to prepare this analysis. This publication has not been reviewed, approved or endorsed by the project owner, its advisers, or any Qualified Person associated with the Project.

The analysis presented is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, technical report, mineral resource estimate, mineral reserve estimate, valuation opinion, fairness opinion, investment research report, securities recommendation, offer to sell, solicitation to buy, or investment advice.

Stormlands Mining is not acting as a broker, dealer, investment adviser, corporate finance adviser, Qualified Person, or securities research provider in connection with this publication.

All model outputs are scenario-based and depend on the assumptions used, including commodity prices, exchange rates, discount rates, capital costs, operating costs, taxes, royalties, production schedules, payability, recoveries, treatment and refining charges, timing assumptions and other inputs. Actual results may differ materially from the scenarios presented. Commodity prices, costs, financing conditions, permitting timelines and project development outcomes are uncertain and subject to change.

Stormlands Mining does not represent or warrant that the information or model outputs are complete, accurate or suitable for any particular purpose. Readers should treat this publication as one source of information only and should conduct their own independent technical, financial, legal, tax and investment due diligence before making any decision.

Neither Stormlands Mining nor any of its directors, officers, employees or advisers accepts any liability for any loss arising from reliance on this publication or the information contained in it.

Stormlands Mining publishes Cerro Caliche Gold Project case study showing modelled NPV more than doubling under March 2026 commodity prices.

Using the data from the most recent technical report, Stormlands rebuilt a base case financial model for Cerro Caliche and then updated the model using March 2026 commodity prices. The Stormlands base case model generated a post-tax NPV of US$222.3 million, closely aligned with the technical report’s reported after-tax NPV of US$224 million. The updated case uses a gold price of US$4,877.40/oz and a silver price of US$74.92/oz. Under this updated commodity price scenario, the modelled project NPV increased to US$475.3 million. This represents an uplift of US$253.0 million, more than doubling the base case valuation.

Life-of-mine revenue increased from US$1.60 billion in the base case to US$2.24 billion under the updated commodity price scenario. Life-of-mine EBITDA increased from US$726.2 million to US$1.35 billion. The modelled payback period improved from 1 year and 7 months to 11 months.

The Cerro Caliche case study also shows the project’s sensitivity to key economic drivers. Stormlands’ analysis indicates that gold price is the dominant value driver, followed by operating costs, recovery assumptions and mine scheduling. A 10% reduction in operating costs increases modelled NPV to US$255 million, while a 10% increase in operating costs reduces NPV to US$189 million. Capital cost sensitivity is more limited, reflecting the relatively modest capital intensity of the proposed heap leach development compared with the project’s life-of-mine revenue base.

Róisín O’Connell, CEO of Stormlands Mining, said:

“Cerro Caliche is a clear example of why mining project valuation needs to be dynamic. The technical report provides the base case, but the economics of a gold project can change materially as commodity prices move. In this published case study, we have only updated the commodity price assumptions, while keeping the mine plan, costs, recoveries, capital and fiscal assumptions unchanged. Even that single change has a material impact on valuation.

“The broader point is that Stormlands models are built to go much further. Once the model is structured, users can test changes across the full project economics — from grades, recoveries, throughput, operating costs and capital costs, through to royalties, fiscal regimes, financing assumptions, inflation and discount rates. By rebuilding the model and making those assumptions dynamic, we can see in real time how the project behaves under current market conditions and where the real value drivers sit.

“The Cerro Caliche model sits between Stormlands’ Rovina Valley and Whistler case studies in terms of commodity price leverage. Updated March 2026 commodity prices increased Cerro Caliche’s modelled NPV by 2.14x, compared with 1.95x for Rovina Valley and 2.33x for Whistler.”

Stormlands’ case study highlights the importance of moving beyond static technical report numbers. Public technical reports contain the data required to build robust economic models, but those models need to be structured, updateable and comparable if they are to support better decision-making.

The updated model keeps the core mine plan, cost, recovery, capital and fiscal assumptions unchanged.

The Cerro Caliche Gold Project is owned by Sonoro Gold Corp. through its Mexican subsidiary, Minera Mar De Plata, S.A. de C.V. The most recent technical report is the updated Mineral Resource Estimate and Preliminary Economic Assessment with an effective date of 4 December 2025.

The Cerro Caliche model is part of the Stormlands Mining Library, a growing repository of dynamic mining valuation models built from public technical reports and company disclosures. The Library is designed to help users analyse, update and compare mining projects across jurisdictions, commodities and development stages.

The full case study is available on the Stormlands Mining website here:

This publication has been prepared by Stormlands Mining Ltd. for informational, educational and illustrative purposes only. It is based on publicly available information, including updated Mineral Resource Estimate and Preliminary Economic Assessment with an effective date of 4 December 2025 , together with independent modelling undertaken by Stormlands Mining.

Stormlands Mining has not been engaged by the project owner or its affiliates to prepare this analysis. This publication has not been reviewed, approved or endorsed by the project owner, its advisers, or any Qualified Person associated with the Project.

The analysis presented is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, technical report, mineral resource estimate, mineral reserve estimate, valuation opinion, fairness opinion, investment research report, securities recommendation, offer to sell, solicitation to buy, or investment advice.

Stormlands Mining is not acting as a broker, dealer, investment adviser, corporate finance adviser, Qualified Person, or securities research provider in connection with this publication.

All model outputs are scenario-based and depend on the assumptions used, including commodity prices, exchange rates, discount rates, capital costs, operating costs, taxes, royalties, production schedules, payability, recoveries, treatment and refining charges, timing assumptions and other inputs. Actual results may differ materially from the scenarios presented. Commodity prices, costs, financing conditions, permitting timelines and project development outcomes are uncertain and subject to change.

Stormlands Mining does not represent or warrant that the information or model outhttps://www.stormlandsmining.com/library/cerro-caliche/puts are complete, accurate or suitable for any particular purpose. Readers should treat this publication as one source of information only and should conduct their own independent technical, financial, legal, tax and investment due diligence before making any decision.

Neither Stormlands Mining nor any of its directors, officers, employees or advisers accepts any liability for any loss arising from reliance on this publication or the information contained in it.

Stormlands Mining publishes independent Dumitru Potok Project case study showing how a Mineral Resource Estimate can be converted into an illustrative economic valuation model.

Illustrative scenario shows how Dumitru Potok economics may respond to March 2026 commodity prices

Stormlands Mining has published a new independent case study on the Dumitru Potok Project in Eastern Serbia, which includes an illustrative economic valuation model showing base case project NPV of US$1.22 billion at a 5% discount rate, with an IRR of 23.3% and payback of 4 years and 3 months after the start of production.

Using its AI-first mining valuation platform, Stormlands has used the publicly available NI 43-101 Mineral Resource Estimate for the Dumitru Potok, Frasen and Rakita North prospects to create an independent illustrative economic model of the project.

Unlike many later-stage mining project case studies, Dumitru Potok does not currently have a published Preliminary Economic Assessment. The NI 43-101 report provides a Mineral Resource Estimate and technical assumptions, but does not publish project economics such as NPV, IRR, payback, capital cost, operating cost or life-of-mine cash flow.

Base case model results

Stormlands has used the public technical information to create an illustrative economic model for the project.

Stormlands’ base case model produces an illustrative post-tax project NPV of US$1.22 billion at a 5% discount rate, with an IRR of 23.3% and payback of 4 years and 3 months after the start of production.

The model also shows life-of-mine revenue of approximately US$10.1 billion, life-of-mine EBITDA of approximately US$4.87 billion, estimated corporate income tax of approximately US$583 million and government royalties of approximately US$501 million.

Updated commodity price scenario

Stormlands also created a second illustrative scenario using updated commodity prices.

The updated illustrative scenario uses March 2026 commodity prices of approximately US$12,499/t copper, US$4,877/oz gold and US$74.91/oz silver, compared with the base case commodity prices of approximately US$8,818/t copper, US$2,600/oz gold and US$26/oz silver.

Using March 2026 commodity prices for copper, gold and silver as an illustrative scenario, Stormlands’ model shows that project NPV increases from US$1.22 billion to US$3.60 billion. IRR increases from 23.3% to 56.9%, while payback improves from 4 years and 3 months to 1 year and 9 months.

Life-of-mine revenue increases from approximately US$10.1 billion in the base case to approximately US$16.8 billion under the updated commodity-price scenario. Life-of-mine EBITDA increases from approximately US$4.87 billion to approximately US$11.23 billion. Estimated corporate income tax also increases materially, from approximately US$583 million to approximately US$1.54 billion.

Government royalties increase from approximately US$501 million to approximately US$835 million under the updated commodity-price scenario.

Value impact drivers

Stormlands’ modelling shows that Dumitru Potok is most sensitive to the overall commodity price deck, with copper and gold acting as the most important individual metal price drivers.

A 10% reduction in the overall commodity price factor reduces NPV to approximately US$845 million, while a 10% increase raises NPV to approximately US$1.6 billion.

Copper is a major individual value driver. A 10% reduction in copper price reduces NPV to approximately US$1.0 billion, while a 10% increase lifts NPV to approximately US$1.4 billion.

Gold also makes a material contribution to value. A 10% reduction in gold price reduces NPV to approximately US$1.1 billion, while a 10% increase raises NPV to approximately US$1.4 billion.

Stormlands’ sensitivity analysis also shows that operating cost and capital cost are important valuation drivers. Stormlands’ heatmap analysis shows that Dumitru Potok remains positive across the tested price and operating-cost scenarios, but with a wide range of valuation outcomes.

At the low end, a combination of weaker prices and higher operating costs reduces NPV to approximately US$124 million. At the high end, stronger prices combined with lower operating costs increases NPV to approximately US$2.3 billion.

Róisín O’Connell, CEO of Stormlands Mining, said:

“Dumitru Potok is a strong example of the gap we see across the mining sector. The technical report gives you tonnes, grade, contained metal, cut-off grade and technical assumptions, but not a project-level economic model. Our view is simple: if a report contains enough information to define a cut-off grade, it already contains the beginning of an economic story.

“This is not about replacing a PEA or a Qualified Person. It is about making the economic question visible earlier. A dynamic model allows investors, project teams and other stakeholders to test how the interpretation of the asset changes as commodity prices, costs and other assumptions move. In this case, the updated commodity-price scenario materially changes the implied value, return profile and payback period. That is the kind of insight that helps move from static technical disclosure to dynamic economic interpretation”

The Dumitru Potok case study is the latest release from the Stormlands Library, a growing repository of interactive mining asset valuation models designed to help users understand the key drivers of mining project economics.

The Dumitru Potok case study is the latest in a series of case studies published in the Stormlands Library. The Library will become a structured source of mining project models, enabling users to screen assets, benchmark projects and test assumptions across commodity prices, operating costs, capital costs, discount rates, taxes, royalties and production scenarios.

The full case study is available through the Stormlands Library at:

Dumitru Project, East Serbia based on NI 43-101 MRE January 2026

The Dumitru Potok case study is based on publicly available information from the NI 43-101 Technical Report and Mineral Resource Estimate for the Dumitru Potok, Frasen and Rakita North prospects in Eastern Serbia dated January 2026, together with independent modelling undertaken by Stormlands Mining.

The technical report reports a total Inferred Mineral Resource of 84.4 million tonnes grading 1.02% copper, 0.97 g/t gold and 6.16 g/t silver.

The purpose of the analysis is to show how structured mining data from a technical report can be converted into a dynamic valuation framework, enabling users to test commodity prices, operating costs, capital costs, discount rates, taxes, royalties and other economic assumptions.

The analysis is illustrative only. It is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, Mineral Reserve estimate or independent technical report.

Canadian Mining Journal

Discovery Alert and

Mining Weekly

of the

Kokiak Copper MPD Project

case study published this week.

Really insightful editorials around the value that Stormlands offers.

See coverage in the

Canadian Mining Journal

and

Discovery Alert

of the

Whistler Project

case study published last week.

Really insightful editorials around the value that Stormlands offers.