MPD Project British Columbia, Canada

The analysis is based on Stormlands Mining’s independent modelling using publicly available technical information, including the NI 43-101 Technical Report and Mineral Resource Estimate December 2025.

Stormlands Mining illustrative economic analysis based on NI 43-101 Mineral Resource Estimate

Introduction

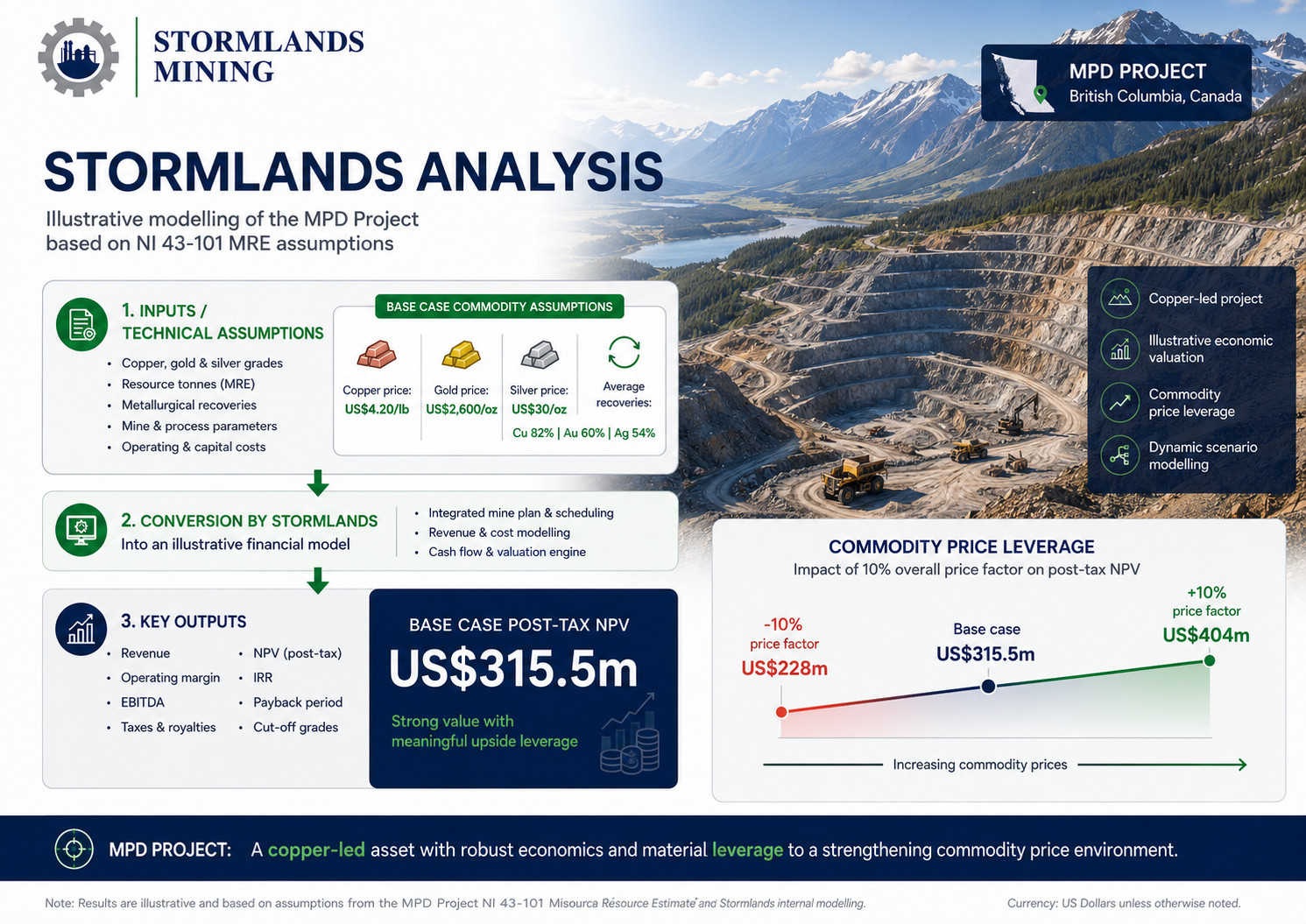

Stormlands Mining’s independent analysis of the MPD Project in British Columbia shows how a publicly available NI 43-101 Mineral Resource Estimate can be converted into an illustrative economic valuation model, even where no economic analysis has been published.

This is the central difference between MPD and many later-stage project case studies. The MPD technical report provides a Mineral Resource Estimate.

Stormlands has used that public technical information as the foundation for an illustrative valuation model, showing how dynamic modelling can help teams understand the possible economic behaviour of a project before a formal economic study is available. The purpose is not to replace a PEA, and the outputs should not be read as formal project economics.

Project NPV

Stormlands’ base case model produces an illustrative post-tax project NPV of US$315.5 million at a 5% discount rate.

The model also shows:

- Post-tax project IRR of 15.5%

- Payback of 6 years and 2 months

- Mine life of 21.3 years

- Life-of-mine revenue of US$2.15 billion

- Life-of-mine EBITDA of US$1.44 billion

- Life-of-mine corporate income tax of US$318 million

These are Stormlands model outputs. They are not published economics from the NI 43-101 report and should not be presented as a PEA, PFS, or DFS.

Stormlands Analysis

Stormlands’ modelling highlights MPD as a copper-led project with material leverage to the commodity price environment.

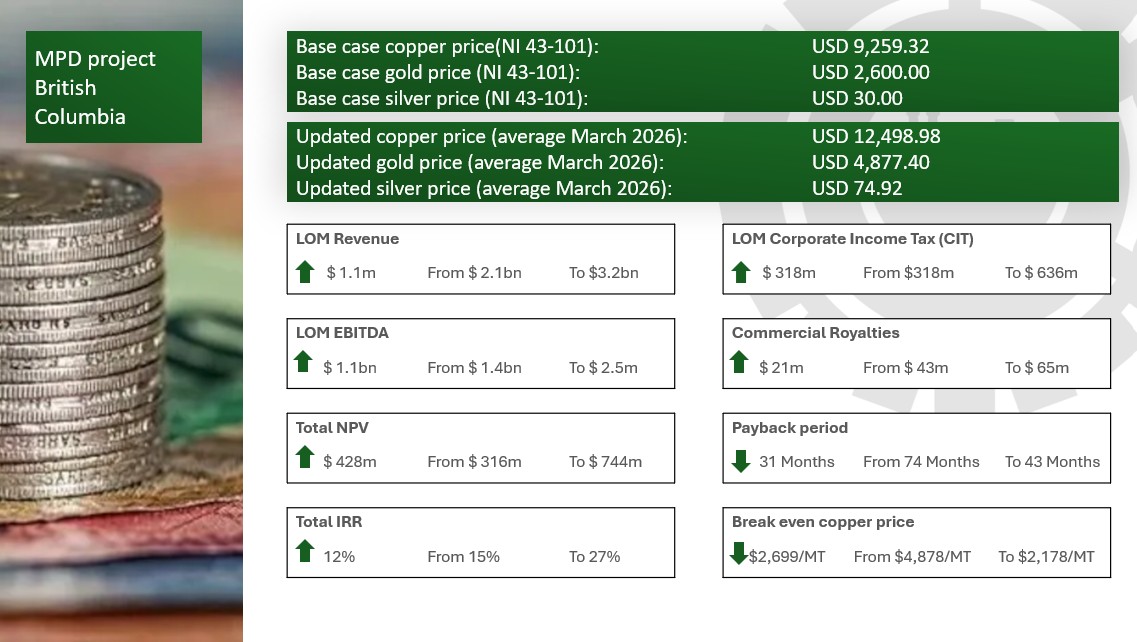

The base case is built around the NI 43-101 MRE assumptions, including copper, gold and silver grades, resource tonnes, metal prices and recovery assumptions. The technical report uses metal prices of US$4.20/lb copper, US$2,600/oz gold and US$30/oz silver. It also references average recoveries of 82% copper, 60% gold and 54% silver.

Stormlands then converts those inputs into an illustrative financial model including revenue, operating margin, EBITDA, tax, royalties, NPV, IRR, payback and cut-off grade metrics.

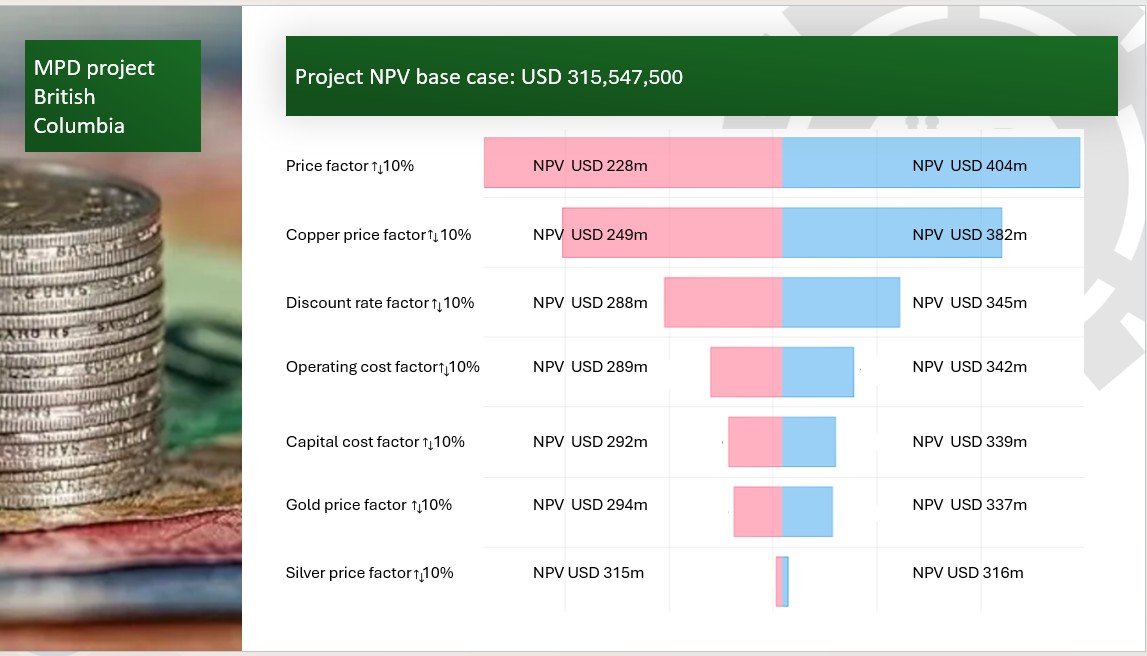

Under the base case, MPD generates an illustrative post-tax NPV of US$315.5 million. The sensitivity analysis shows that a 10% reduction in the overall price factor reduces NPV to US$228 million, while a 10% increase raises NPV to US$404 million.

That range shows the project’s price leverage. MPD is not simply a static copper-gold-silver resource. Its implied valuation changes materially as the price deck changes.

Key Highlights

- Base case NPV of US$315.5 million

Using the MRE-based technical assumptions, the Stormlands model produces an illustrative post-tax NPV of US$315.5 million and an IRR of 15.5%. - Updated commodity prices materially increase value

Under the updated March 2026 commodity-price scenario, project NPV increases from US$315.5 million to US$743.6 million. That is an uplift of US$428 million, or around 136%. - Project returns improve significantly under stronger metals prices

The updated price scenario increases IRR from 15.5% to 27.7%. - Payback improves from 6 years and 2 months to 3 years and 7 months.

This is one of the clearest valuation insights from the model. Stronger commodity prices do not just increase NPV. They also shorten capital recovery and materially change the risk-reward profile. - Revenue and EBITDA uplift are substantial

Life-of-mine revenue increases from US$2.15 billion to US$3.23 billion.

Life-of-mine EBITDA increases from US$1.44 billion to US$2.50 billion. - Uplift driven purely by price

Because the underlying resource, mine life, CAPEX and OPEX assumptions are unchanged, the uplift is driven by price. This shows the power of dynamic modelling: the technical report remains the same, but the economic interpretation changes.

The upside benefits government and royalty holders - Corporate income tax

Higher metal prices increase estimated life-of-mine corporate income tax from US$318 million to US$636 million. - Commercial Royalties

Commercial royalties increase from US$43 million to US$65 million.

This is an important point as it shows that higher commodity prices increase the value flowing to government and royalty holders as well as investors. - MPD remains copper-led, but gold becomes more important

MPD should be presented primarily as a copper project. Copper is the dominant individual price driver in the sensitivity analysis.

However, under the updated commodity-price scenario, gold becomes a more important contributor to overall project value. Gold revenue increases materially and becomes a larger part of the revenue mix. - Silver increases sharply in price but remains immaterial to the overall project valuation.

- Stormlands creates an economic model where no economic analysis previously existed.

The MPD case study demonstrates one of the core uses of the Stormlands platform: creating a structured, auditable, illustrative economic model from a technical report that does not itself contain project economics. The NI 43-101 provides the technical foundation. Stormlands turns that foundation into an investment-style model with NPV, IRR, payback, life-of-mine revenue, EBITDA, tax, royalties and margin outputs

Value Drivers

- Price factor

The strongest value driver in the Stormlands model is the overall commodity price factor.

A 10% decrease in the overall price factor reduces NPV to US$228 million. A 10% increase raises NPV to US$404 million.

This is a swing of US$176 million around the base case.

The insight is straightforward: MPD is highly exposed to the commodity price environment. The same tonnes and grades produce materially different valuation outcomes depending on the price deck applied.

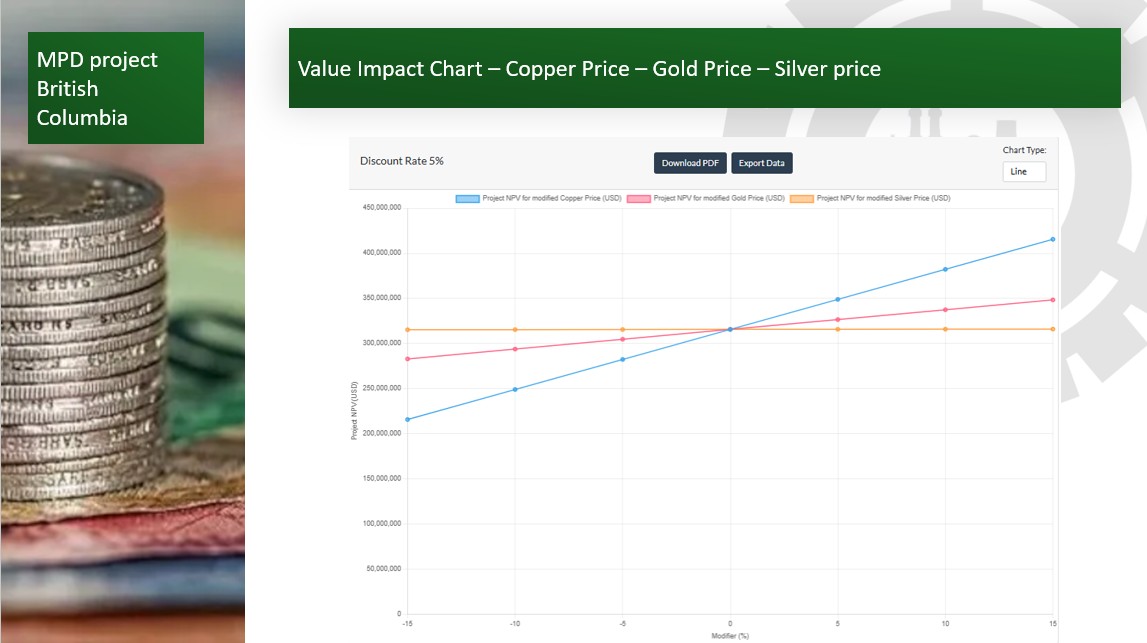

- Copper price

Copper is the dominant individual metal price driver. A 10% reduction in copper price reduces NPV to US$249 million, while a 10% increase lifts NPV to US$382 million. This confirms that MPD behaves economically as a copper-led project. Gold and silver contribute by-product value, but copper is the main driver of valuation.

- Gold price

Gold is a meaningful secondary value driver. A 10% reduction in gold price reduces NPV to US$294 million, while a 10% increase raises NPV to US$337 million. Gold does not dominate the valuation, but it provides useful support.

- Operating cost

Operating cost is an important controllable driver, but it is less influential than price. A 10% increase in operating cost reduces NPV to US$289 million, while a 10% reduction increases NPV to US$342 million.

- Capital cost

Capital cost has a moderate effect on valuation. A 10% increase in capital cost reduces NPV to US$292 million, while a 10% reduction increases NPV to US$339 million. This indicates that development CAPEX is important, but the project’s value is not driven by capital cost alone.

- Discount rate

The discount-rate sensitivity is material, but it is not the principal valuation driver. A 10% reduction in the discount-rate factor increases NPV to US$345 million, while a 10% increase reduces NPV to US$288 million. This shows that the timing and risk profile of future cash flows matter, but the model remains more sensitive to commodity prices than to discount-rate changes.

- Silver price

Silver has limited impact on total project value. A 10% change in silver price produces only a small movement in NPV, from US$315 million to US$316 million.

This is an important modelling insight. MPD is a copper-gold-silver project geologically, but not all metals contribute equally to value. The model helps separate headline polymetallic disclosure from the actual economic drivers.

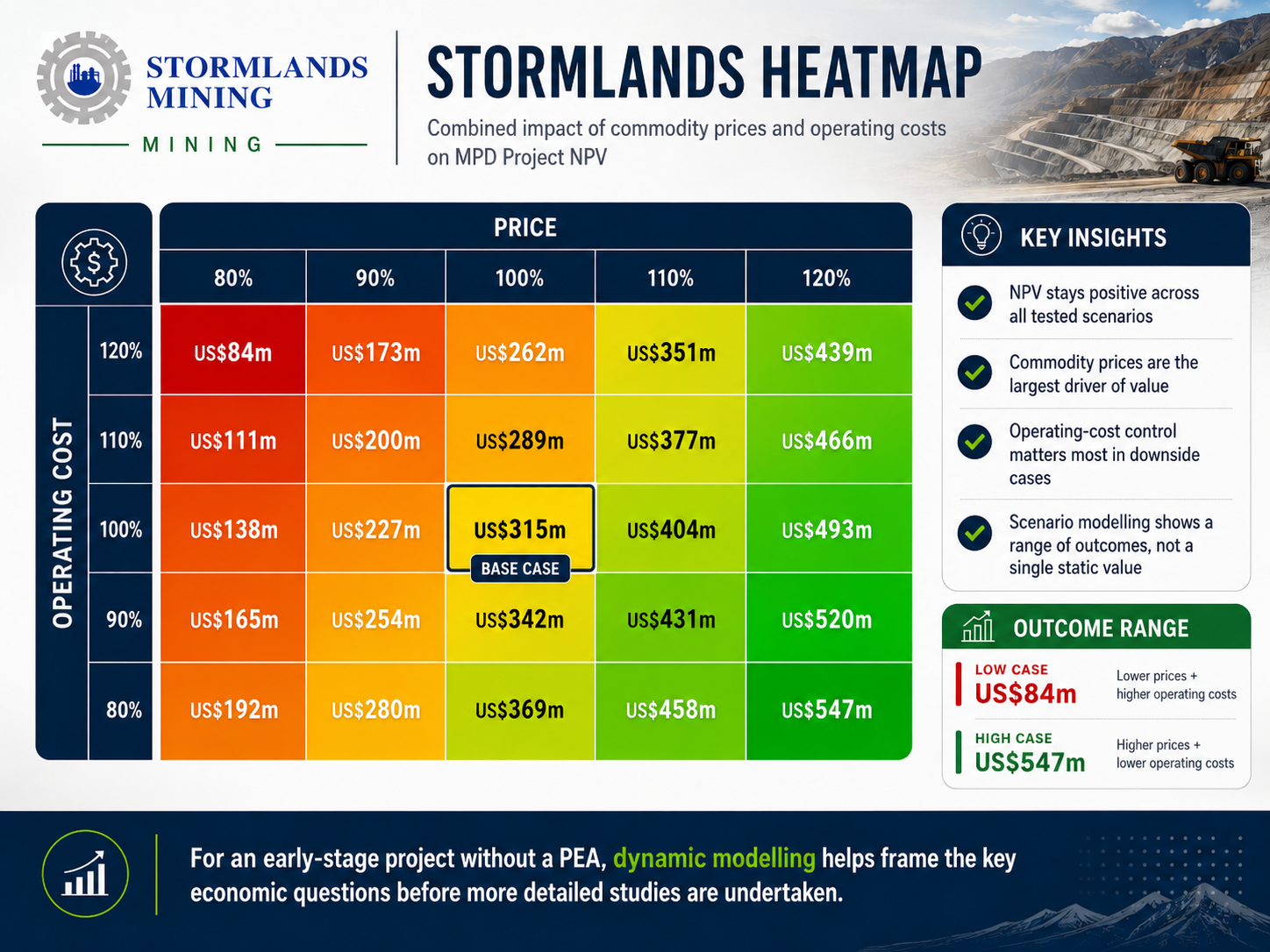

Heatmap

Stormlands’ heatmap across price and operating cost shows the combined impact of changes to commodity prices and operating costs on project NPV.

The model remains positive across the tested matrix, but the range of outcomes is wide. At the low end, a combination of weaker prices and higher operating costs reduces NPV to US$84 million. At the high end, stronger prices combined with lower operating costs increases NPV to US$547 million.

This is a powerful case-study output because it shows that the question is not simply whether MPD has a single project value. The better question is how the valuation behaves under changing market and cost conditions.

The heatmap reinforces three conclusions:

- First, commodity prices are the largest driver of value.

- Second, operating-cost control remains important, particularly in downside cases.

- Third, dynamic scenario modelling helps users understand the range of possible outcomes rather than relying on a single static number.

For an early-stage project without a PEA, this is especially useful. It gives project teams a way to frame the key economic questions before committing to more detailed technical and engineering studies.

Updated commodity prices

Updated Commodity Prices

The updated commodity-price scenario is the most striking result of the MPD analysis.

The base case uses:

- Copper: US$9,259/t

- Gold: US$2,600/oz

- Silver: US$30/oz

Stormlands then applies March 2026 commodity prices:

- Copper: US$12,499/t

- Gold: US$4,877/oz

- Silver: US$74.91/oz

Under this updated price scenario:

- Life-of-mine revenue increases from US$2.15 billion to US$3.23 billion.

- Life-of-mine EBITDA increases from US$1.44 billion to US$2.50 billion.

- Post-tax NPV increases from US$315.5 million to US$743.6 million.

- IRR increases from 15.5% to 27.7%.

- Payback improves from 6 years and 2 months to 3 years and 7 months.

This is the core insight from the MPD case study. The underlying resource does not change. The modelled ore body size remains 82.9 million tonnes. The mine life remains 21.3 years. CAPEX and OPEX are unchanged. What changes is the market environment.

That change materially alters the project’s implied economic profile.

The updated commodity-price scenario improves the value of each tonne mined.

- Net smelter return increases from US$25.93/t ore to US$38.97/t ore.

- Cash operating margin increases from US$17.93/t ore to US$30.97/t ore.

- Operating margin increases from 69.2% to 79.5%.

- The updated price scenario also reduces the modelled break-even copper price from US$4,878/t to US$2,179/t.

- The break-even copper cut-off grade falls from 0.11% Cu to 0.08% Cu.

- The mine design cut-off grade falls from 0.17% Cu to 0.12% Cu.

Summary

The MPD Project is not being presented here as a completed economic study.

It is being used to show what becomes possible when structured mining data is extracted from a technical report and converted into a dynamic valuation model.

The NI 43-101 Mineral Resource Estimate provides the geological and technical base. Stormlands then creates an illustrative economic framework that allows users to ask:

- What is the implied scale of the opport|unity?

- What mine life could be supported by the Indicated Resource?

- Which metals drive the valuation?

- How sensitive is the project to copper, gold and silver prices?

- How much do operating costs and capital costs matter?

- How does the valuation change under current commodity prices?

- What happens to tax, royalties and payback?

- Where should future technical work be focused before a formal PEA?

This is the value of the Stormlands approach. It does not turn an MRE into a PEA. It does not remove the need for engineering, metallurgical, geotechnical, environmental or mine-planning work.

But it does create a disciplined, transparent and repeatable way to move from technical disclosure to economic questions.

Conclusion

Stormlands’ illustrative model of the MPD Project shows a copper-led project with meaningful economic sensitivity to commodity prices.

Under the base case, the model produces an illustrative post-tax NPV of US$315.5 million, IRR of 15.5%, and payback of 6 years and 2 months.

Under the March 2026 commodity-price scenario, NPV increases to US$743.6 million, IRR improves to 27.7%, and payback shortens to 3 years and 7 months.

The sensitivity analysis and heatmap show that MPD is most exposed to the overall price deck and copper price, while operating cost, capital cost and gold price also influence value. Silver has limited impact on total valuation.

The broader insight is more important than the individual numbers.

MPD demonstrates how Stormlands can take a Mineral Resource Estimate and create an illustrative economic model before a formal PEA exists. This gives analysts and project teams a way to test scenarios, understand value drivers and identify the technical assumptions that matter most.

For early-stage mining projects, this is where dynamic modelling can add real value: not by replacing formal technical studies, but by helping decision-makers understand which questions should be asked next.

About Stormlands

Stormlands Mining is an AI-first valuation and analytics platform for mining assets and critical minerals. The platform helps investors, banks, mining corporate development teams, M&A advisers and other stakeholders turn technical disclosures into interactive valuation models in minutes, rather than days or weeks. The valuation models are accessible over multiple platforms to all users, enabling the user to interact directly with the data to facilitate scenario-planning.

The platform enables users to build discounted cash flow models at scale, test commodity price, capex, opex, tax, royalty rates, discount-rates and production scenarios, and compare opportunities and scenarios.

Stormlands is now using its technology to build the Stormlands Library: a global repository of mining asset valuation models. It has moved beyond a tool for analysts building individual models and is developing a data layer for the mining industry: a structured source of valuation models and illustrative scenarios. This creates a new way for investors, corporates, professional advisers, financial-market users and public-policy stakeholders to screen assets, benchmark projects and understand the key drivers of mining asset economics.

Disclaimer

This analysis has been prepared by Stormlands Mining using publicly available information from the MPD Project NI 43-101 Technical Report and Mineral Resource Estimate, together with Stormlands’ own independent modelling assumptions.

The analysis is illustrative only. It is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, Mineral Reserve estimate or independent technical report. It has not been prepared on behalf of the project owner and has not been reviewed or approved by the project owner.

The model outputs are Stormlands-generated illustrative estimates only. They should not be interpreted as demonstrated economic viability. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Future technical work, including mine planning, metallurgical testing, engineering, environmental studies, permitting, capital-cost estimation and operating-cost estimation, would be required before any formal economic conclusions could be drawn.

More information

Download the full Kodiak Copper Corp. MPD Project case study

View MPD Project on YouTube