Whistler Gold-Copper project, Alaska

The analysis is based on Stormlands Mining’s independent modelling using publicly available technical information, including the NI 43-101 Technical Report and Preliminary Economic Assessment March 2026. The purpose of the analysis is to illustrate how the project’s economics may change under different commodity-price, operating-cost, capital-cost and discount-rate scenarios.

Stormlands Mining’s independent analysis of the Whistler Gold-Copper Project shows a large-scale gold-copper development project with strong price leverage, particularly to gold, copper and broader commodity-price assumptions.

Project NPV

Stormlands’ base case model, using the technical-report and PEA assumptions, produces a post-tax project NPV of approximately US$2.02 billion at a 5% discount rate. The model also shows a post-tax project IRR of approximately 31.9%, with payback occurring around 2 years and 6 months after the start of production.

The project economics are supported by a long mine life, substantial life-of-mine revenue, meaningful by-product value and strong operating margins. In the Stormlands base case, life-of-mine revenue is approximately US$10.9 billion, life-of-mine EBITDA is approximately US$5.9 billion, and life-of-mine corporate income tax is approximately US$1.03 billion.

Key Highlights

- Whistler at PEA prices

Using the base case commodity-price assumptions, the Stormlands model produces a post-tax project NPV of US$2.02 billion, an IRR of 32%, and payback of 2 years and 6 months. - Current commodity prices increase project value

Current commodity-price illustrative scenario materially increases project value. Under this scenario, project NPV increases from US$2.02 billion to US$4.71 billion. - Project returns improve significantly under stronger metals prices

Under the updated commodity-price illustrative scenario, project IRR increases from 32% to 61%, while payback improves from 30 months to 19 months. - Revenue and EBITDA uplift are substantial

Revenue increases from US$10.9 billion to US$16.1 billion, while EBITDA increases from US$5.9 billion to US$11.0 billion under new illustrative scenario. - The upside benefits government

Higher commodity prices materially increase estimated corporate income tax from US$1.03 bn to US$2.18 bn. - Whistler is highly sensitive to gold and copper price assumptions

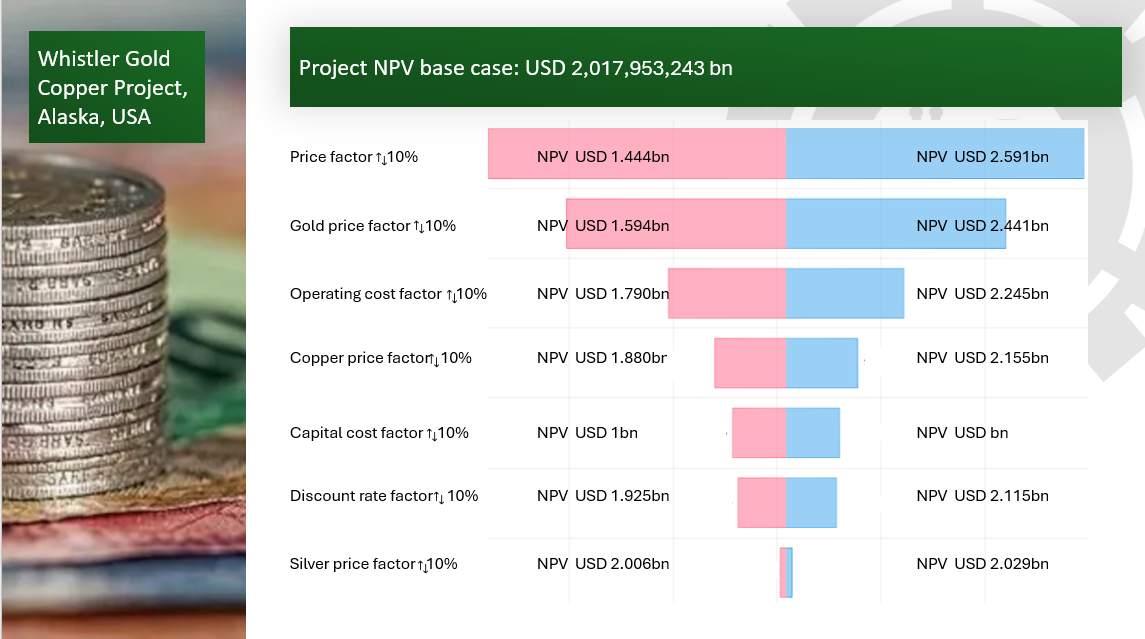

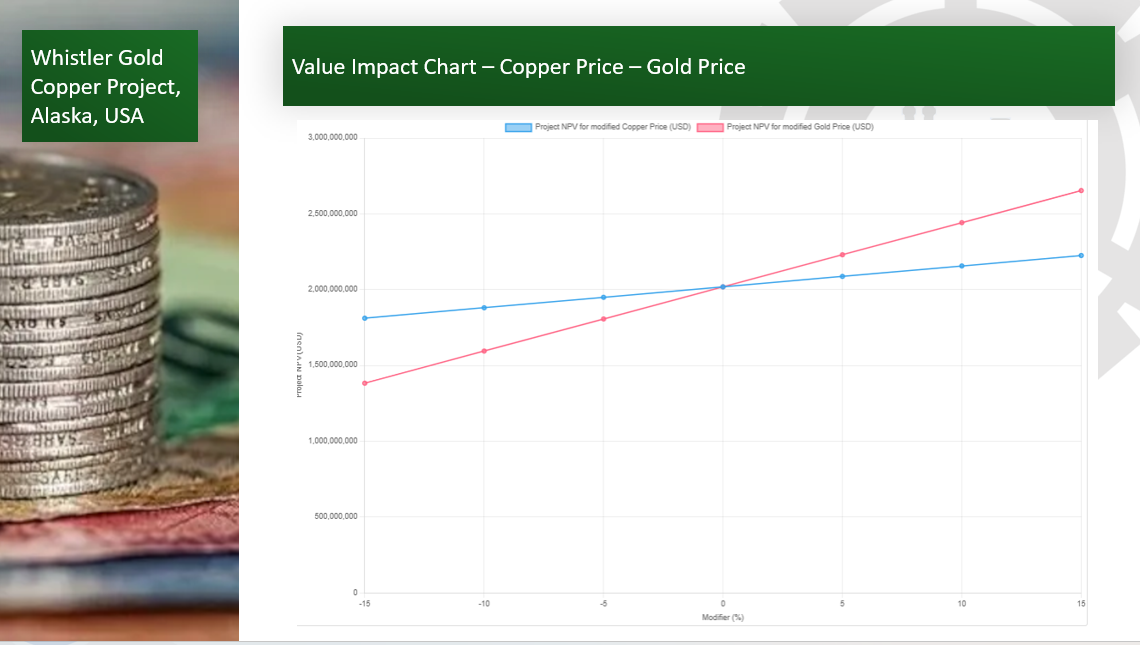

The sensitivity analysis shows that both gold and copper materially influence valuation. A 10% increase in gold price lifts NPV to US$2.16 billion, while a 10% increase in copper price lifts NPV to US$2.12 billion. The overall price-factor sensitivity is larger still, demonstrating the combined effect of stronger metal prices across the revenue basket.

Stormlands Sensitivity Analysis

Stormlands’ modelling highlights Whistler as a price-leveraged gold-copper project. The model is most sensitive to changes in commodity prices and operating costs, with gold and copper price assumptions acting as the dominant external value drivers.

Under the base case, Whistler generates a project NPV of approximately US$2.02 billion. The sensitivity analysis shows that a 10% reduction in the overall price factor reduces NPV to approximately US$1.44 billion, while a 10% increase raises NPV to approximately US$2.59 billion. This range demonstrates the extent to which project value is exposed to the commodity-price environment.

The value impact chart and heatmap reinforce the same conclusion: Whistler remains meaningfully positive across a broad range of price and cost cases, but its valuation expands significantly in stronger price scenarios.

Updated Commodity Prices

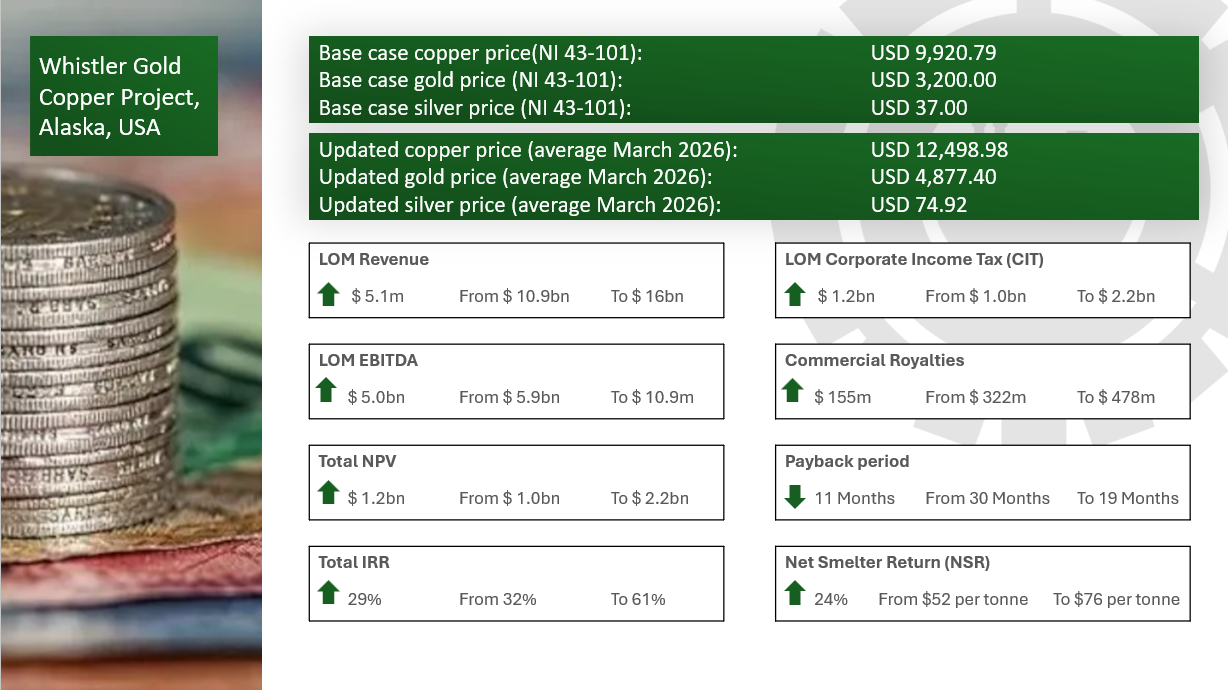

The updated commodity-price scenario is the most striking result. The base case uses copper at US$9,920.79/t, gold at US$3,200/oz, and silver at US$37.50/oz. Stormlands then uses current commodity prices in a new illustrative scenario using copper at US$12,498.98/t, gold at US$4,877.40/oz, and silver at US$74.92/oz.

Under this new illustrative scenario, revenue increases from US$10.9 billion to US$16.1 billion. Life-of-mine EBITDA increases from US$5.9 billion to US$11.0 billion. Total project NPV increases from US$2.02 billion to US$4.71 billion, while IRR increases from 32% to approximately 61.%.

The increase in value is substantial. The model shows that Whistler is not merely a robust project under base case assumptions; it is a project with significant embedded leverage to stronger gold and copper prices.

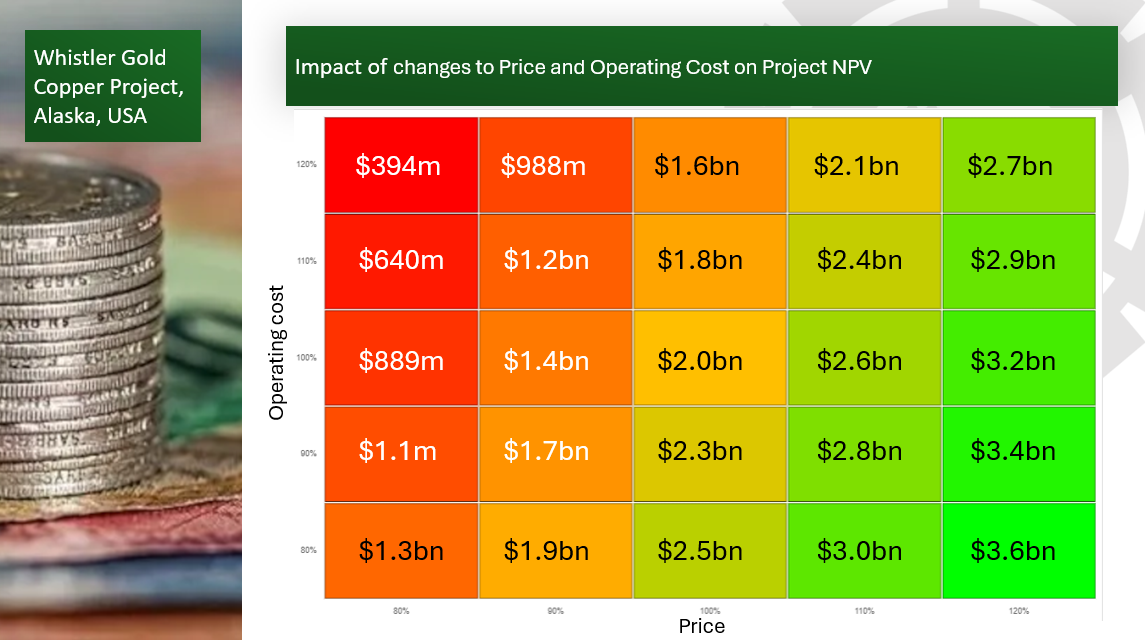

Stormlands Heatmap

Stormlands’ heatmap shows the impact of changes to price and operating cost on project NPV. The model remains positive under the lower-price and higher-cost cases, but the upside increases sharply as commodity prices improve and operating costs fall.

At the lower end of the heatmap, adverse combinations of weaker prices and higher operating costs reduce NPV materially. At the upper end, stronger prices combined with lower operating costs lift project NPV into the multi-billion-dollar range.

This reinforces the central insight from the sensitivity analysis: Whistler’s value is highly responsive to commodity prices, while operating-cost discipline remains an important protection against downside scenarios.

Price Sensitivity

Higher commodity prices materially change the risk-reward profile. In the base case, the project shows payback of approximately 30 months. Under the current commodity-price illustrative scenario, payback improves to 19 months, reducing the period of capital exposure and accelerating the return of invested capital.

Net smelter return increases from US$52/t ore to US$76/t ore. Cash operating margin also improves materially, increasing from US$31/t ore to US$55/t ore. Operating margin percentage increases from 59.7% to 72.7%.

The benefit of stronger commodity prices is also visible in tax outcomes. Corporate income tax increases from US$1.03 billion to US$2.18 billion, demonstrating that the upside is shared between investors and the host government.

The published technical information and PEA assumptions already support a substantial development case. However, the current metal-price environment materially enhances Whistler’s attractiveness. Stormlands’ updated commodity-price scenario converts an already valuable project into a substantially higher-value, faster-paying gold-copper asset.

Summary

The published NI 43-101 Technical Report and PEA March 2026 already supports a robust development case, but the current metal-price environment materially enhances the project’s attractiveness. The project appears to offer leveraged exposure to elevated gold and copper prices, with the March 2026 price scenario converting an already strong project into a substantially higher-value, faster-paying asset.

About Stormlands

Stormlands Mining is an AI-first valuation and analytics platform for mining assets and critical minerals. The platform helps investors, banks, mining corporate development teams, M&A advisers and other stakeholders turn technical disclosures into interactive valuation models in minutes, rather than days or weeks. The valuation models are accessible over multiple platforms to all levels users, enabling the user to interact directly with the data to facilitate scenario-planning.

The platform enables users to build discounted cash flow models at scale, test commodity price, capex, opex, tax, royalty rates, discount-rates and production scenarios, and compare opportunities and scenarios.

Stormlands is now using its technology to build the Stormlands Library: a global repository of mining asset valuation models. It has moved beyond a tool for analysts building individual models and is developing a data layer for the mining industry: a structured source of valuation models and illustrative scenarios. This creates a new way for investors, corporates, professional advisers, financial-market users and public-policy stakeholders to screen assets, benchmark projects and understand the key drivers of mining asset economics.

Disclaimer

This publication has been prepared by Stormlands Mining Ltd. for informational, educational and illustrative purposes only. It is based on publicly available information, including the NI 43-101 Technical Report and Preliminary Economic Assessment March 2026, together with independent modelling undertaken by Stormlands Mining.

Stormlands Mining has not been engaged by US Gold Mining Inc. or its affiliates to prepare this analysis. This publication has not been reviewed, approved or endorsed by US Gold Mining Inc., its advisers, or any Qualified Person associated with the Project.

The analysis presented is not a technical report, mineral resource estimate, mineral reserve estimate, valuation opinion, fairness opinion, investment research report, securities recommendation, offer to sell, solicitation to buy, or investment advice. Stormlands Mining is not acting as a broker, dealer, investment adviser, corporate finance adviser, Qualified Person, or securities research provider in connection with this publication.

All model outputs are scenario-based and depend on the assumptions used, including commodity prices, exchange rates, discount rates, capital costs, operating costs, taxes, royalties, production schedules, payability, recoveries, treatment and refining charges, timing assumptions and other inputs. Actual results may differ materially from the scenarios presented. Commodity prices, costs, financing conditions, permitting timelines and project development outcomes are uncertain and subject to change.

Stormlands Mining does not represent or warrant that the information or model outputs are complete, accurate or suitable for any particular purpose. Readers should treat this publication as one source of information only and should conduct their own independent technical, financial, legal, tax and investment due diligence before making any decision.

Neither Stormlands Mining nor any of its directors, officers, employees or advisers accepts any liability for any loss arising from reliance on this publication or the information contained in it.