Cerro Caliche Gold Project, Sonora, Mexico

The analysis of Cerro Caliche Gold Project, Sonora, Mexico, is based on Stormlands Mining’s independent modelling using publicly available technical information, including the updated Mineral Resource Estimate and Preliminary Economic Assessment with an effective date of 4 December 2025.

Introduction

The Cerro Caliche Gold Project is a gold-silver development project located in Sonora, Mexico. The project is owned by Sonoro Gold Corp. through its Mexican subsidiary, Minera Mar De Plata, S.A. de C.V. The project is supported by an updated Mineral Resource Estimate and Preliminary Economic Assessment with an effective date of 4 December 2025.

The technical report outlines a conventional open-pit, heap leach development scenario based on shallow gold and silver mineralisation across multiple mineralised zones. The proposed operation processes 52.8 million tonnes of heap leach feed over a 10-year mine life, with average grades of 0.36 g/t gold and 3.7 g/t silver. The project assumes gold recovery of 72% and silver recovery of 27%, producing 436,000 payable ounces of gold and 1.7 million payable ounces of silver.

Using the data disclosed in the technical report, Stormlands rebuilt a dynamic financial model for the Cerro Caliche Project. The objective was to demonstrate how technical report data can be extracted, structured and converted into a working valuation model that can be updated, tested and compared under different market assumptions.

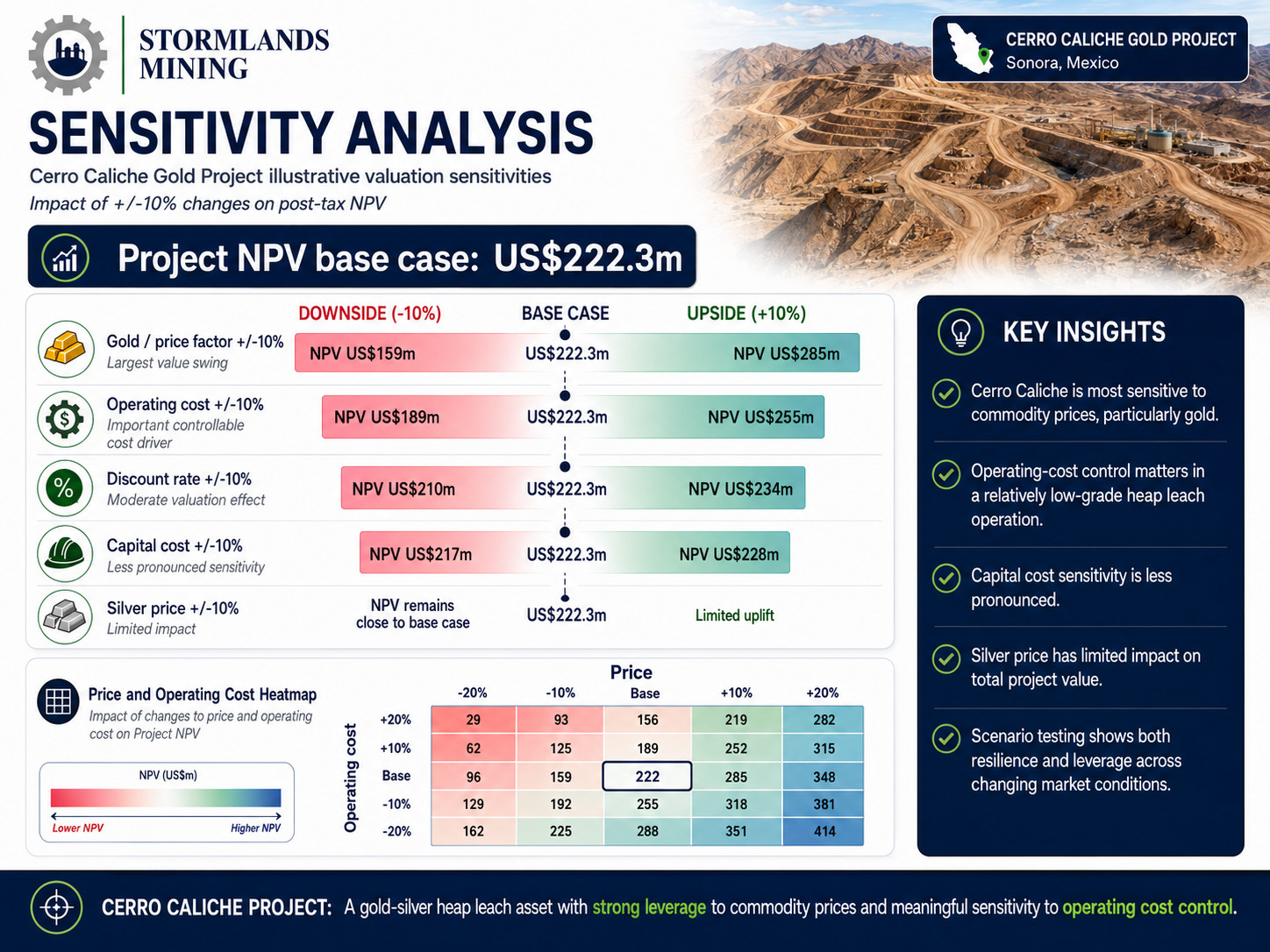

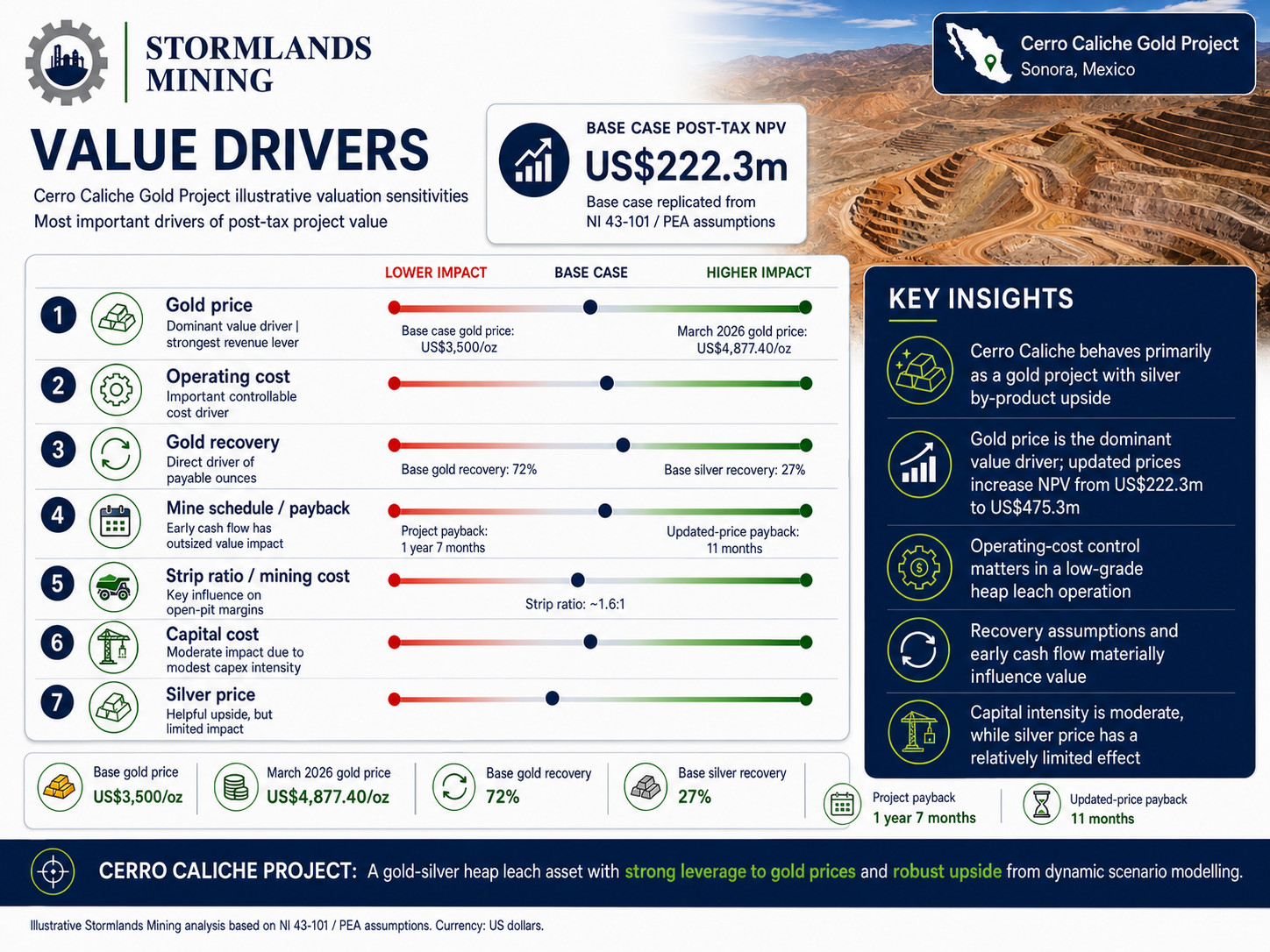

The base case model was built using the assumptions in the technical report, including gold at US$3,500/oz and silver at US$48/oz. On this basis, the Stormlands model generated a post-tax NPV of US$222.3 million, closely aligned with the technical report’s reported after-tax NPV of US$224 million.

This confirms the ability of the Stormlands workflow to recreate a public technical report valuation model and produce a dynamic version that can then be used for scenario analysis, price updates, sensitivity testing and investment screening.

Base Case Model

The Stormlands base case model reflects the published development assumptions for Cerro Caliche.

The model includes an open-pit mining operation, heap leach processing route, gold and silver revenue streams, government and commercial royalty payments, operating costs, capital costs, sustaining capital, corporate income tax and discounted post-tax free cash flow.

Under the base case assumptions, Cerro Caliche generates life-of-mine revenue of US$1.60 billion. Life-of-mine operating costs are US$819.6 million, with total capital expenditure, including sustaining capital, of US$109.2 million.

The resulting life-of-mine EBITDA is US$726.2 million. After royalties, tax and capital costs, the Stormlands model generates a post-tax NPV of US$222.3 million and a payback period of 1 year and 7 months.

This base case provides the starting point for scenario analysis. It reflects the project economics as disclosed in the technical report and provides a structured model that can be updated in real time as commodity prices, costs, development assumptions or fiscal terms change.

Updating the model to March 2026 commodity prices

The base case uses the commodity prices from NI43-101:

- Gold price: US$3,500.00/oz

- Silver price: US$48.00/oz

Stormlands then updated the Cerro Caliche model using March 2026 commodity price assumptions.

The updated commodity price case uses:

- Gold price: US$4,877.40/oz

- Silver price: US$74.92/oz

All other core operating, capital and fiscal assumptions were held constant. This isolates the impact of updated commodity prices on the valuation of the project.

Under the updated price scenario, life-of-mine revenue increases from US$1.60 billion to US$2.24 billion. This represents an increase of US$644 million in life-of-mine revenue.

The impact on project cash flow is significant. Life-of-mine EBITDA increases from US$726.2 million to US$1.35 billion. Post-tax net operating profit after tax increases from US$385.6 million to US$775.9 million.

The project NPV increases from US$222.3 million in the base case to US$475.3 million under the updated commodity price case. This is an increase of US$253.0 million, or more than double the base case NPV.

The payback period also improves materially, reducing from 1 year and 7 months in the base case to 11 months under the updated commodity price case.

Why this matters

The Cerro Caliche case study demonstrates the importance of being able to update mining project valuations quickly and consistently.

A technical report provides the underlying development case. However, the economic valuation of a project can change materially as commodity prices move. In the case of Cerro Caliche, updating the model from the report’s base case metal prices to March 2026 commodity price assumptions increases the project NPV by US$253 million.

The updated case does not change the geology, mine plan, processing route or cost assumptions. It simply updates the commodity price inputs. The result is a materially different valuation profile.

This is particularly important for gold projects in a rising gold price environment. Projects that may already appear robust at technical report prices can become significantly more valuable when modelled using current market prices. Conversely, dynamic models also allow investors, companies and advisers to test downside scenarios, cost escalation, discount rate sensitivity and margin pressure.

Value Drivers

Stormlands also tested the sensitivity of the Cerro Caliche valuation to changes in key assumptions.

The sensitivity analysis shows that the project is most sensitive to commodity prices, particularly gold. A 10% change in the gold price has a much larger impact on project NPV than an equivalent 10% change in capital costs or silver price.

Operating costs are also an important driver of value. A 10% decrease in operating costs increases NPV to US$255 million, while a 10% increase in operating costs reduces NPV to US$189 million. This reflects the importance of mining, processing and G&A cost control in a relatively low-grade heap leach operation.

Capital cost sensitivity is less pronounced. A 10% reduction in capital costs increases NPV to US$228 million, while a 10% increase reduces NPV to US$217 million. This is consistent with the project’s relatively modest initial capital requirement compared with its life-of-mine revenue base.

The price and operating cost heatmap demonstrates the range of possible outcomes. Under the downside scenario of lower prices and higher operating costs, NPV falls materially. Under the upside scenario of higher prices and lower operating costs, NPV increases significantly. This type of scenario testing allows users to understand not only the base case valuation, but the resilience and leverage of the project under different market and operating conditions.

Commercial interpretation

Cerro Caliche is a useful example of how a public technical report can be converted into a dynamic valuation model.

The base case demonstrates that the project has a positive post-tax NPV at the technical report assumptions. The updated commodity price case demonstrates the project’s leverage to higher gold and silver prices. The sensitivity analysis shows that gold price and operating costs are the most important valuation drivers.

For investors, this type of model helps frame the valuation discussion. It allows users to move beyond static technical report numbers and test how the project behaves under different commodity price, cost and discount rate assumptions.

For mining companies, it provides a structured way to communicate the project’s value drivers and update economics as market conditions change.

For advisers and analysts, it provides a repeatable workflow for converting technical disclosure into comparable project-level financial models.

Key Highlights

Base case project economics are already robust. Using the assumptions disclosed in the technical report, the Stormlands base case model generates a post-tax NPV8% of approximately US$222.3 million, closely aligned with the technical report’s reported after-tax NPV8% of approximately US$224 million.

Cerro Caliche is highly leveraged to gold and silver prices. When the model is updated to March 2026 commodity prices, while keeping the core mine plan, operating cost, capital cost and fiscal assumptions unchanged, project NPV8% increases to approximately US$475.3 million.

Updated commodity prices more than double the modelled project value. The move from the base case to the March 2026 price scenario increases NPV by approximately US$253 million, demonstrating the scale of value uplift that can emerge when a static technical report model is refreshed with current market prices.

Life-of-mine revenue increases materially. In the base case, Cerro Caliche generates approximately US$1.60 billion of life-of-mine revenue. Under the updated commodity price scenario, life-of-mine revenue increases to approximately US$2.24 billion, an uplift of approximately US$644 million.

Operating leverage is significant. Because the updated price scenario holds operating and capital costs constant, a large portion of the additional revenue flows through to project cash flow. Life-of-mine EBITDA increases from approximately US$726.2 million in the base case to approximately US$1.35 billion under the updated price case.

Payback improves sharply. The base case payback period is approximately 1 year and 7 months from the start of production. Under the updated commodity price case, payback improves to approximately 11 months, reflecting the stronger early cash flow profile at higher gold and silver prices.

Gold is the primary valuation driver. The sensitivity analysis shows that Cerro Caliche is most sensitive to changes in the gold price. A 10% change in the gold price has a much greater impact on project NPV than an equivalent 10% change in capital costs or silver price.

Operating costs remain an important risk and value lever. A 10% reduction in operating costs increases NPV to approximately US$255 million, while a 10% increase in operating costs reduces NPV to approximately US$189 million. This highlights the importance of mining, processing and G&A cost control in a heap leach operation.

Capital cost sensitivity is more limited. A 10% decrease in capital costs increases NPV to approximately US$228 million, while a 10% increase reduces NPV to approximately US$217 million. This reflects the relatively modest initial capital requirement compared with the project’s life-of-mine revenue base.

The project shows strong upside in a higher-price environment. The price and operating cost heatmap shows a wide valuation range, with NPV increasing materially under higher price and lower cost scenarios. This makes Cerro Caliche a strong example of why dynamic scenario modelling is important for gold development projects.

Stormlands converts a static technical report into a live valuation tool. The case study demonstrates how public technical disclosure can be transformed into a dynamic model that can be updated for commodity prices, sensitivity analysis, downside testing and project comparison.

Conclusion

The Cerro Caliche case study demonstrates the value of turning public technical report data into a dynamic, scenario-ready valuation model.

Using the technical report assumptions, Stormlands recreated a base case valuation of US$222.3 million NPV. Updating the model to March 2026 commodity prices increased the project NPV to US$475.3 million.

That uplift of US$253.0 million illustrates how sensitive gold project valuations can be to commodity price assumptions, and why static technical report numbers can quickly become outdated in fast-moving markets.

Stormlands enables users to extract data from technical reports, build valuation models, update commodity prices, test sensitivities and compare projects in a consistent and transparent way.

The Cerro Caliche model is part of the Stormlands Mining Library, a growing repository of dynamic mining valuation models built from public technical reports and company disclosures.

About Stormlands

Stormlands Mining is an AI-first valuation and analytics platform for mining assets and critical minerals. The platform enables users turn technical disclosures into interactive valuation models in minutes, rather than days or weeks. The valuation models are accessible over multiple platforms to all levels users, enabling the user to interact directly with the data to facilitate scenario-planning.

The platform enables users to build discounted cash flow models at scale, test commodity price, capex, opex, tax, royalty rates, discount-rates and production scenarios, and compare opportunities and scenarios.

Stormlands uses its own technology to build the Stormlands Library: a global repository of mining asset valuation models. It has moved beyond a tool for analysts building individual models and is developing a data layer for the mining industry: a structured source of valuation models and illustrative scenarios. This creates a new way for investors, corporates, professional advisers, financial-market users and public-policy stakeholders to screen assets, benchmark projects and understand the key drivers of mining asset economics.

Important Notice

This publication has been prepared by Stormlands Mining Ltd. for informational, educational and illustrative purposes only. It is based on publicly available information, including updated Mineral Resource Estimate and Preliminary Economic Assessment with an effective date of 4 December 2025 , together with independent modelling undertaken by Stormlands Mining.

Stormlands Mining has not been engaged by the project owner or its affiliates to prepare this analysis. This publication has not been reviewed, approved or endorsed by the project owner, its advisers, or any Qualified Person associated with the Project.

The analysis presented is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, technical report, mineral resource estimate, mineral reserve estimate, valuation opinion, fairness opinion, investment research report, securities recommendation, offer to sell, solicitation to buy, or investment advice.

Stormlands Mining is not acting as a broker, dealer, investment adviser, corporate finance adviser, Qualified Person, or securities research provider in connection with this publication.

All model outputs are scenario-based and depend on the assumptions used, including commodity prices, exchange rates, discount rates, capital costs, operating costs, taxes, royalties, production schedules, payability, recoveries, treatment and refining charges, timing assumptions and other inputs. Actual results may differ materially from the scenarios presented. Commodity prices, costs, financing conditions, permitting timelines and project development outcomes are uncertain and subject to change.

Stormlands Mining does not represent or warrant that the information or model outputs are complete, accurate or suitable for any particular purpose. Readers should treat this publication as one source of information only and should conduct their own independent technical, financial, legal, tax and investment due diligence before making any decision.

Neither Stormlands Mining nor any of its directors, officers, employees or advisers accepts any liability for any loss arising from reliance on this publication or the information contained in it.