Stormlands Mining publishes independent case study on Illinois Creek Gold Project – Illustrative scenario establishes project NPV of US$226.2m and shows current commodity prices nearly double NPV to US$448.6 million

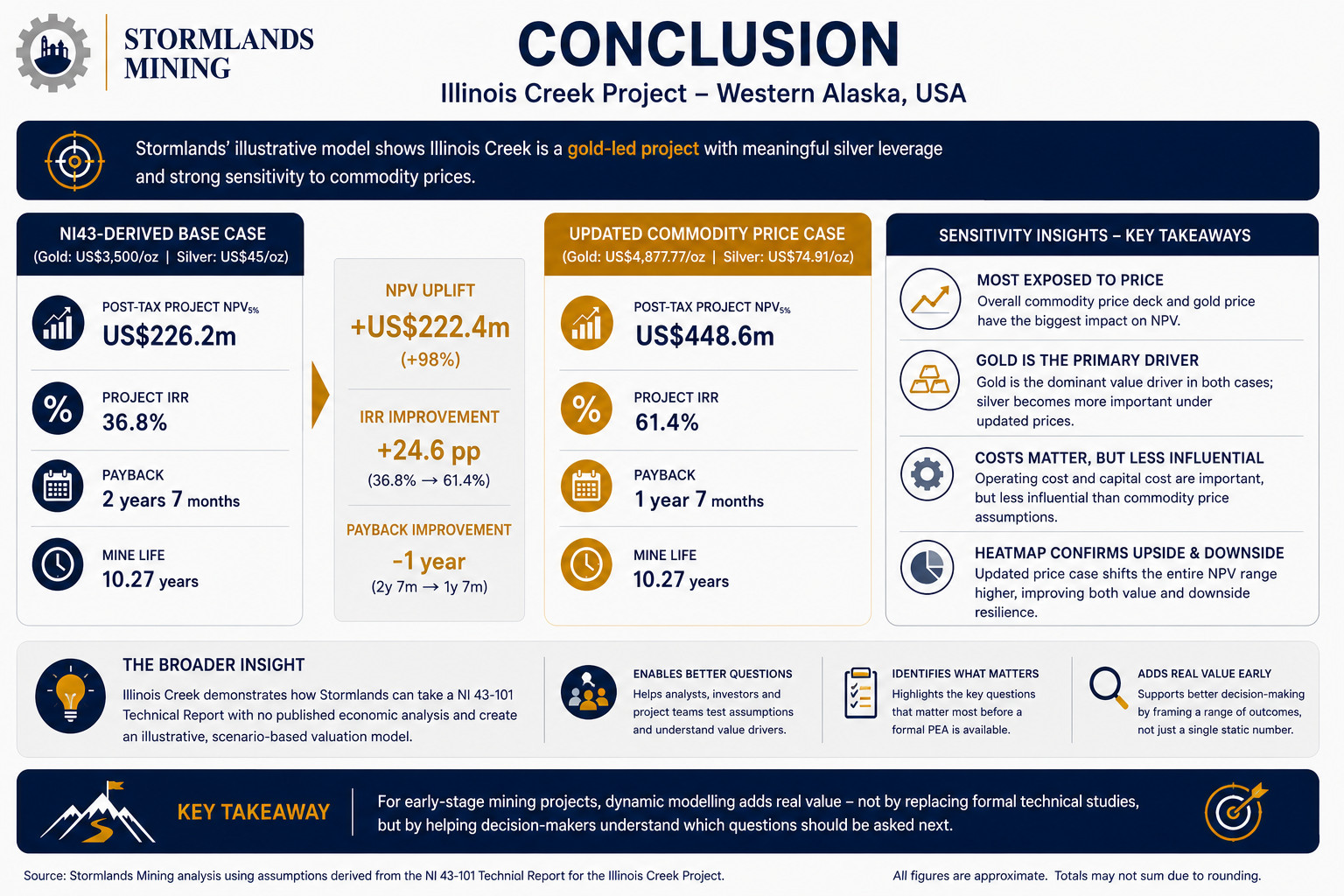

Stormlands Mining has published a new independent case study on the Illinois Creek Project in western Alaska, USA. Using data extracted from the NI 43-101 Technical Report effective data January 2026, the Stormlands model generates an post-tax project Net Present Value (NPV) of US$226.2 million at an 8% discount rate, with a post-tax project Internal Rate of Return (IRR) of 36.8% and a payback period of 2 years and 7 months.

The model also generates:

-

- Life-of-mine revenue of US$1.15 billion

- Life-of-mine EBITDA of US$805 million

- Life-of-mine corporate income tax of US$190 million

- Mine life of 10.27 years

- Initial capital requirement of US$150 million

Stormlands then updated the model using March 2026 commodity prices while holding the core physical and cost assumptions constant, including mine life, production output, capital costs, operating costs and discount rate.

Under this updated commodity price scenario, modelled post-tax project NPV increases from US$226.2 million to US$448.6 million, representing an uplift of approximately US$222 million, or 98%.

Project IRR increases from 36.8% to 61.4%, while payback improves from 2 years and 7 months to 1 year and 7 months.

Life-of-mine revenue increases from US$1.15 billion to US$1.69 billion. Life-of-mine EBITDA increases from US$805 million to US$1.32 billion. Modelled life-of-mine corporate income tax increases from US$190 million to US$345 million, while modelled government royalties increase from US$34.6 million to US$50.6 million.

The underlying resource, mine life, capital cost, operating cost and discount rate remain unchanged between the two scenarios. The uplift is driven by the commodity price environment.

Value drivers

- Stormlands’ sensitivity analysis shows that the overall commodity price factor is the strongest value driver in the Illinois Creek model.

- In the NI 43-101-derived base case, a 10% increase or decrease in the overall commodity price factor moves project NPV from US$178 million to US$274 million. In the updated commodity price model, the same sensitivity moves project NPV from US$378 million to US$519 million.

- Gold is the dominant individual metal price driver. In the NI 43-101-derived model, a 10% increase or decrease in gold price moves project NPV from US$190 million to US$262 million. In the updated commodity price model, the same gold price sensitivity moves project NPV from US$398 million to US$499 million.

- Silver is a meaningful secondary driver, and its contribution increases under the updated commodity price case. In the updated model, a 10% increase or decrease in silver price moves project NPV from US$429 million to US$469 million.

- Operating cost and capital cost remain important, but the model shows that Illinois Creek’s valuation is more sensitive to commodity prices than to cost variation within the tested ranges.

Gold-led project with meaningful silver leverage

- The Stormlands model shows Illinois Creek as a gold-led project, with silver providing a meaningful secondary contribution.

- In the NI 43-101-derived base case, gold contributes approximately US$867 million of payable revenue, while silver contributes approximately US$286 million. In the updated commodity price case, gold revenue increases to approximately US$1.21 billion, while silver revenue increases to approximately US$478 million.

- The revenue mix shifts from approximately 75% gold and 25% silver in the base case to approximately 72% gold and 28% silver in the updated commodity price case. Gold remains the dominant revenue driver, but silver becomes more important under the updated price deck.

The Illinois Creek model forms part of the Stormlands Mining Library, a growing repository of mining asset valuation models built from public technical reports and company disclosures.

The case study demonstrates how a technical report with no published economic analysis can be converted into an scenario-driven valuation model. It allows users to ask practical economic questions before a formal PEA is available in order to understand the value drivers that influence the project economics.