Stormlands Mining publishes independent case study on Bralorne Gold Project

Illustrative scenario establishes project NPV of US$181.8 million at a 5% discount rate and shows current commodity prices push the project NPV to US$339.4 million

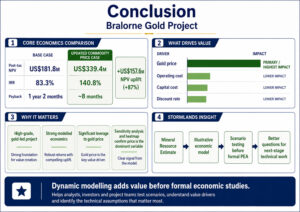

Dublin, Ireland – [13 July 2026] – Stormlands Mining has published a new independent case study on the Bralorne Gold Project in British Columbia, Canada. Using data extracted from the NI 43-101 Technical Report on the Mineral Resource Estimate dated June 26 2026, Stormlands developed an illustrative economic model that generates a post-tax project Net Present Value (NPV) of US$181.8 million at a 5% discount rate, with a post-tax project Internal Rate of Return (IRR) of 83.3% and a payback period of 1 year and 2 months.

The model also generates:

- Life-of-mine revenue of US$551.9 million

- Life-of-mine EBITDA of US$411.6 million

- Life-of-mine post-tax free cash flow of US$232.6 million

- Life-of-mine corporate income tax of US$99.7 million

- Life-of-mine commercial royalties of US$25.9 million

- Mine life of 5.37 years

Updated Commodity Prices

Stormlands then updated the model using a updated gold price to the average of March 2026, while holding all other core assumptions constant, including mine life, production schedule, recoveries, operating costs, capital costs, sustaining capital, royalties, fiscal assumptions and discount rate.

Under this scenario, the gold price increases from US$3,200/oz to US$4,877/oz. Project NPV increases from US$181.8 million to US$339.4 million, representing an uplift of approximately US$157.6 million, or 87%, compared with the base case.

Project IRR increases from 83.3% to 140.8%, while payback improves from 1 year and 2 months to approximately 8 months.

Life-of-mine revenue increases from US$551.9 million to US$841.2 million. Life-of-mine EBITDA increases from US$411.6 million to US$687.2 million, while life-of-mine post-tax free cash flow increases from US$232.6 million to US$425.6 million.

The underlying resource base, mine life, production profile, capital costs and operating costs remain unchanged between the two scenarios.

The uplift is therefore driven entirely by the updated gold price.

Roisin O’Connell, CEO of Stormlands Mining, said: “The mining industry has a valuation problem. Billions of dollars are invested in exploration long before a PEA exists, yet investors are expected to value projects using little more than drill results, presentations and intuition. We believe that approach belongs to another era.

AI and analytics now make it possible to create transparent, structured economic models directly from technical report data, moving valuation years earlier in the asset lifecycle. That doesn’t replace formal engineering studies, it complements them. It gives the market a way to connect geology to economics, exploration to value, and technical disclosure to investment decisions while projects are still being shaped.”

Margin expansion

The discounted cash flow comparison shows that stronger gold prices materially improve project margins.

Life-of-mine EBITDA increases from US$411.6 million to US$687.2 million.

Net smelter return increases from US$851.66/t ore to US$1,298.09/t ore. Cash operating margin increases from US$694.13/t ore to US$1,140.56/t ore, while operating margin percentage increases from 81.5% to 87.9%.

This means that the same physical mine plan generates substantially higher profitability without any change to mining, processing, capital or operating cost assumptions.

Value drivers

Stormlands’ sensitivity analysis shows that gold price is overwhelmingly the dominant driver of project value.

In the base case model, the Project NPV is approximately US$181.8 million. Sensitising price moves NPV from approximately US$152 million to US$212 million.

By comparison, operating cost sensitivity moves NPV from approximately US$176 million to US$188 million. Capital cost sensitivity moves NPV from approximately US$177 million to US$186 million, while discount-rate sensitivity produces a similar range.

The general Price Factor and Gold Price Factor produce the same valuation movement, confirming that Bralorne behaves economically as a gold project.

Operating cost is important, but it is not the dominant value driver. Capital cost sensitivity is relatively limited, reflecting the strength of the project’s modelled margins and the short, front-loaded mine life.

Heatmap analysis

The price and operating cost heatmap, modelling 20% increases and decreases in gold price and operating cost, provides one of the strongest insights from the Bralorne case study.

Under the base case model, Project NPV is approximately US$182 million at 100% gold price and 100% operating cost.

In the downside scenario of 20% lower gold price and 20% higher operating cost, Project NPV remains positive at approximately US$109 million.

In the upside scenario of 20% higher gold price and 20% lower operating cost, Project NPV increases to approximately US$254 million.

The heatmap demonstrates that the project remains positive across all tested scenarios. It also shows that gold price has substantially greater influence on valuation than operating costs.

One notable insight is that a 10% increase in gold price more than offsets a 20% increase in operating cost. At 110% gold price and 120% operating cost, Project NPV is approximately US$200 million, still above the base case.

Economic resilience

One of the most important findings from the case study is the project’s modelled resilience.

Even under scenarios combining lower gold prices and higher operating costs, the model continues to generate positive value.

This suggests that the project’s illustrative economics are supported by the combination of high grade, strong net smelter return per tonne, strong operating margins and a short payback profile.

The Bralorne Gold Project is owned by Talisker Resources Ltd. Stormlands modelled the project using public technical disclosure and independent analysis.