Kandiolé Gold Project, Kéniéba Cercle, Kayes Region, western Mali

The analysis of the Kandiolé Gold Project, Kéniéba Cercle, Kayes Region, western Mali, is based on Stormlands Mining’s independent modelling using publicly available technical information, including the NI 43-101 Preliminary Economic Assessment with an effective date of 27 February 2026.

Introduction

The Kandiolé Gold Project is a gold development project owned by Roscan Gold Corporation. Stormlands modelled the project using the NI 43-101 Preliminary Economic Assessment with an effective date of 27 February 2026.

The project has been evaluated as a single-commodity gold project, with revenue generated from gold doré production.

Using the disclosed mine plan and economic assumptions, Stormlands rebuilt a dynamic discounted cash flow model for Kandiolé. The Stormlands model includes mine production, ore production, gold doré production, gold doré revenue, operating costs, capital costs, sustaining capital, commercial royalties, government royalties, corporate income tax, post-tax free cash flow, NPV, IRR, payback and other data points.

Two scenarios were modelled and compared:

- A base case model extracted from the NI 43-101 technical report assumptions, using a gold price of US$3,100/oz.

- An updated commodity price case using the average of March 2026 gold price: US$4,877.40/oz.

All other core assumptions were held constant between the two cases. The updated commodity price case therefore isolates the impact of higher gold price assumptions on the project’s valuation.

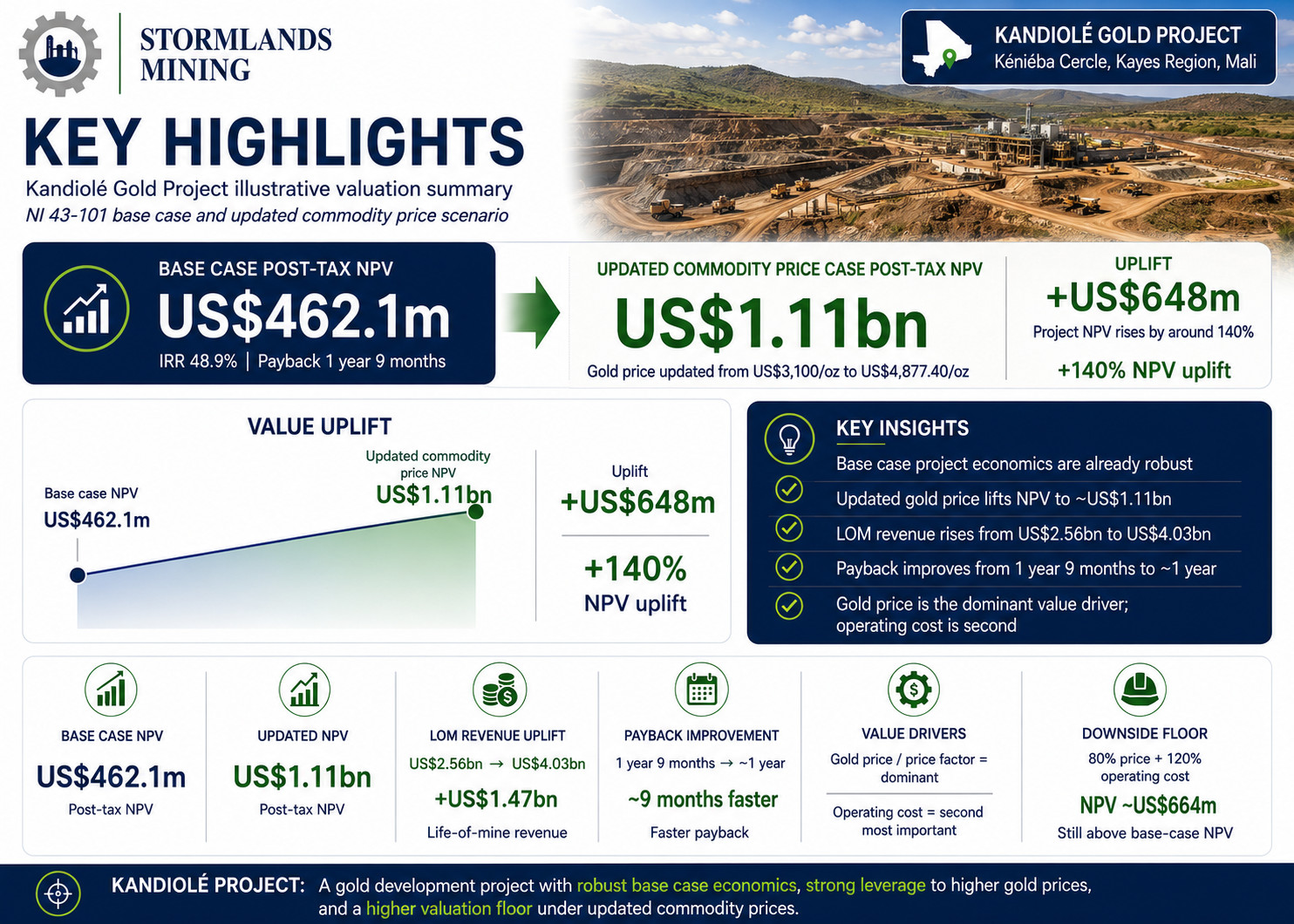

Key Highlights

Base case project economics are already robust. Using the NI 43-101 baseassumptions, the Stormlands model generates a post-tax project NPV of approximately US$462.1 million, with an IRR of 48.9% and payback of approximately 1 year and 9 months.

Kandiolé is highly leveraged to the gold price. Updating the model from a gold price of US$3,100/oz to US$4,877.40/oz, while keeping mine life, grade, opex, capex and fiscal assumptions unchanged, increases project NPV to approximately US$1.11 billion.

The updated price case adds approximately US$648 million of NPV. The increase from US$462.1 million to US$1.11 billion represents an uplift of approximately US$648 million, or around 140%.

Life-of-mine revenue increases materially. Revenue increases from approximately US$2.56 billion in the NI 43-101 basecase to approximately US$4.03 billion in the updated commodity price case, an uplift of approximately US$1.47 billion.

The same physical project generates a very different valuation. Ore body size, mine output, grade, mine life, operating cost and capital cost are unchanged. The valuation uplift is driven almost entirely by repricing the same payable gold production at updated commodity prices.

Operating leverage is significant. Life-of-mine EBITDA increases from approximately US$1.31 billion to approximately US$2.64 billion, more than doubling under the updated price scenario.

NPV increases faster than revenue. Revenue increases by approximately 57%, while post-tax NPV increases by approximately 140%. This demonstrates the project’s strong operational gearing to gold price.

Payback improves sharply. The NI 43-101 base case pays back in approximately 1 year and 9 months. Under the updated commodity price case, payback improves to approximately 1 year.

Government revenues increase materially. Government royalties and corporate income tax increase from approximately US$554 million in the NI 43-101 base case to approximately US$1.12 billion in the updated commodity price case.

Gold price is the dominant value driver. Sensitivity analysis shows that the price factor and gold price factor have the largest effect on NPV. Operating cost is the second most important driver, while capital cost and discount rate have more limited impact.

The updated case has a much higher valuation floor. In the heatmap downside case of 80% price and 120% operating cost, the updated commodity price model still generates an NPV of approximately US$664 million, higher than the NI 43-101 base case NPV of approximately US$462 million.

Stormlands converts static disclosure into a dynamic valuation tool. The Kandiolé case study demonstrates how a public technical report model can be recreated, updated for commodity prices, tested for sensitivities and compared across scenarios.

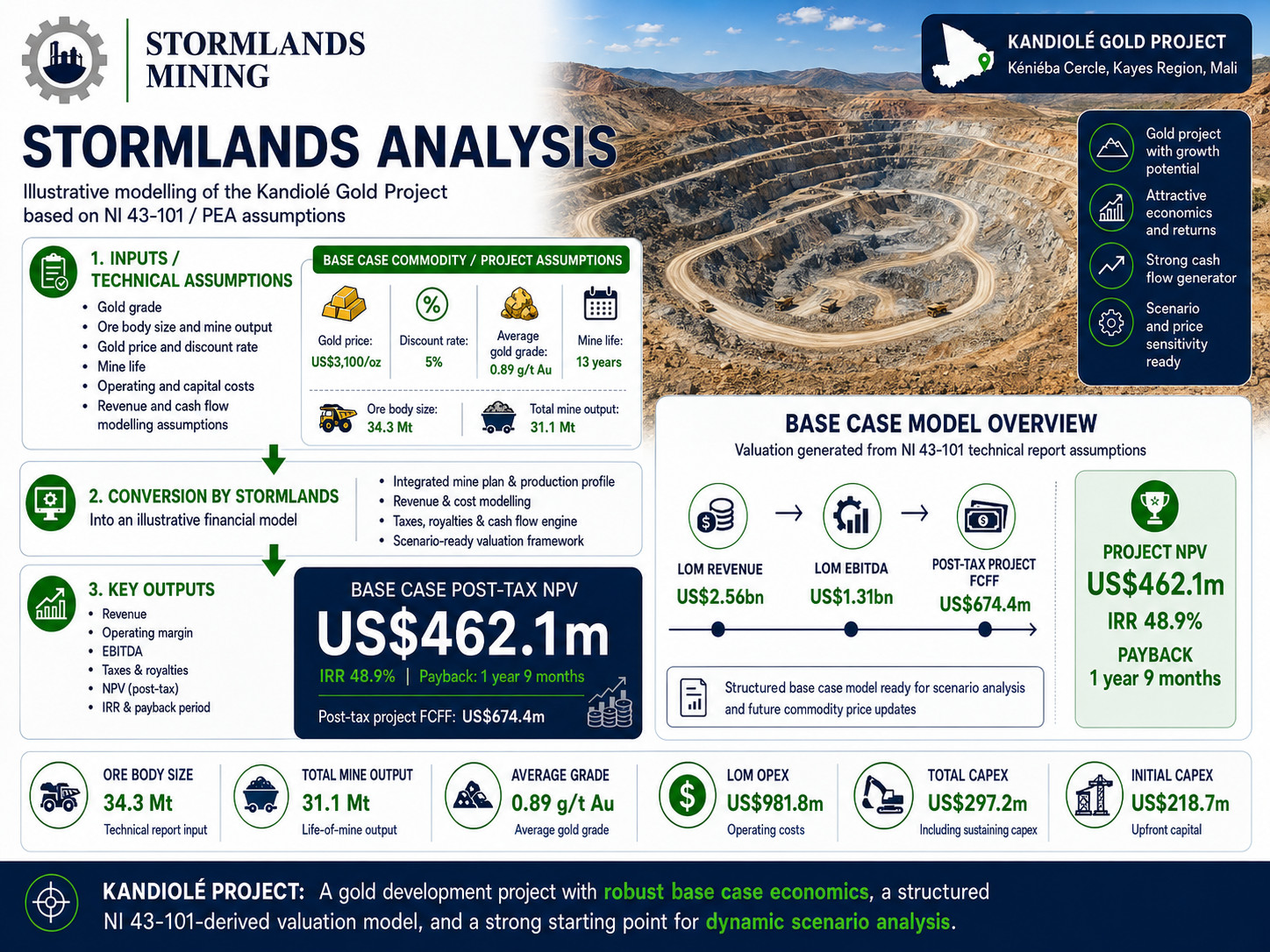

Base case model

The Stormlands base case model reflects the NI 43-101 development assumptions for Kandiolé.

The model assumes an ore body size of approximately 34.3 million tonnes, total mine output of approximately 31.1 million tonnes, an average gold grade of 0.89 g/t, and a mine life of 13 years.

The model uses a gold price of US$3,100/oz and a discount rate of 5%. Life-of-mine operating costs are approximately US$981.8 million, with total capital expenditure including sustaining capital of approximately US$297.2 million. Initial capex is approximately US$218.7 million.

Under these assumptions, Kandiolé generates life-of-mine revenue of approximately US$2.56 billion. Life-of-mine EBITDA is approximately US$1.31 billion, and post-tax project free cash flow is approximately US$674.4 million.

The resulting post-tax project NPV is approximately US$462.1 million, with an IRR of 48.9% and payback of approximately 1 year and 9 months.

This base case provides the starting point for scenario analysis. It reflects the valuation generated using the technical report assumptions and provides a structured model that can then be updated as commodity prices, costs, fiscal terms or development assumptions change.

Updated Commodity Price Case

Stormlands then updated the Kandiolé model using an updated gold price assumption of US$4,877.40/oz.

All other core assumptions were held constant, including mine life, production profile, ore grade, operating cost, capital cost, sustaining capital and fiscal assumptions. This isolates the impact of updated gold prices on the project valuation.

Under the updated commodity price scenario, life-of-mine revenue increases from approximately US$2.56 billion to approximately US$4.03 billion. This represents an increase of approximately US$1.47 billion, or 57%.

The impact on cash flow is significant. Life-of-mine EBITDA increases from approximately US$1.31 billion to approximately US$2.64 billion. Post-tax project free cash flow increases from approximately US$674.4 million to approximately US$1.57 billion.

The project NPV increases from approximately US$462.1 million in the NI 43-101 basecase to approximately US$1.11 billion under the updated commodity price case. This is an increase of approximately US$648 million, or approximately 140%.

The project IRR increases from 48.9% to 97.0%, while payback improves from approximately 1 year and 9 months to approximately 1 year.

Revenue Report Insights

The revenue report confirms that Kandiolé is effectively a gold doré revenue model. The price factor and gold price factor move together, indicating that there is no material by-product revenue offset in the model.

The payable gold production profile remains unchanged between the two scenarios. The updated commodity price case does not assume higher production, higher grade, improved recovery or a longer mine life. It simply reprices the same payable gold production at a higher gold price.

This is important because it demonstrates the value of dynamic model updating. The physical project remains the same, but the valuation context changes materially.

In the NI 43-101 base case, the model generates life-of-mine revenue of approximately US$2.56 billion. In the updated commodity price case, life-of-mine revenue increases to approximately US$4.03 billion.

Net smelter return increases from approximately US$82.52/t ore to approximately US$129.88/t ore. Cash operating margin increases from approximately US$50.90/t ore to approximately US$98.26/t ore.

This means the project moves from a strong margin asset to a very high margin asset under updated commodity price assumptions.

Margin and cash flow expansion

The updated commodity price case materially improves the quality of the project’s cash flows.

Life-of-mine EBITDA increases from approximately US$1.31 billion to approximately US$2.64 billion. EBITDA margin increases from approximately 51% of revenue to approximately 65% of revenue.

Operating margin also improves materially. The operating margin percentage increases from approximately 61.7% to approximately 75.7%.

This margin expansion occurs because operating and capital costs are unchanged in the updated commodity price case. As gold price increases, a significant portion of the additional revenue flows through to operating margin, EBITDA and post-tax free cash flow.

This is one of the most important conclusions from the model: Kandiolé has strong operational leverage to gold price.

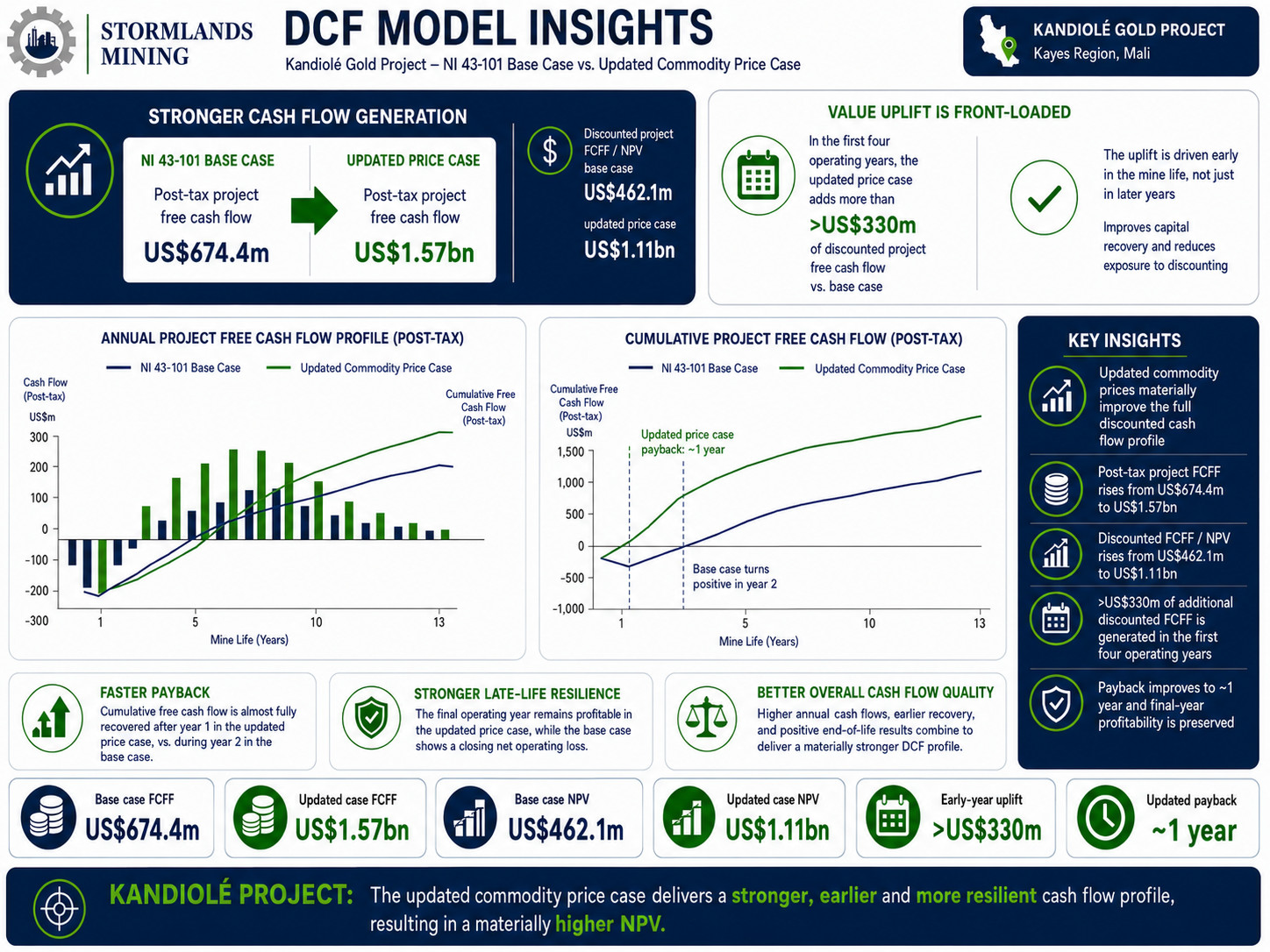

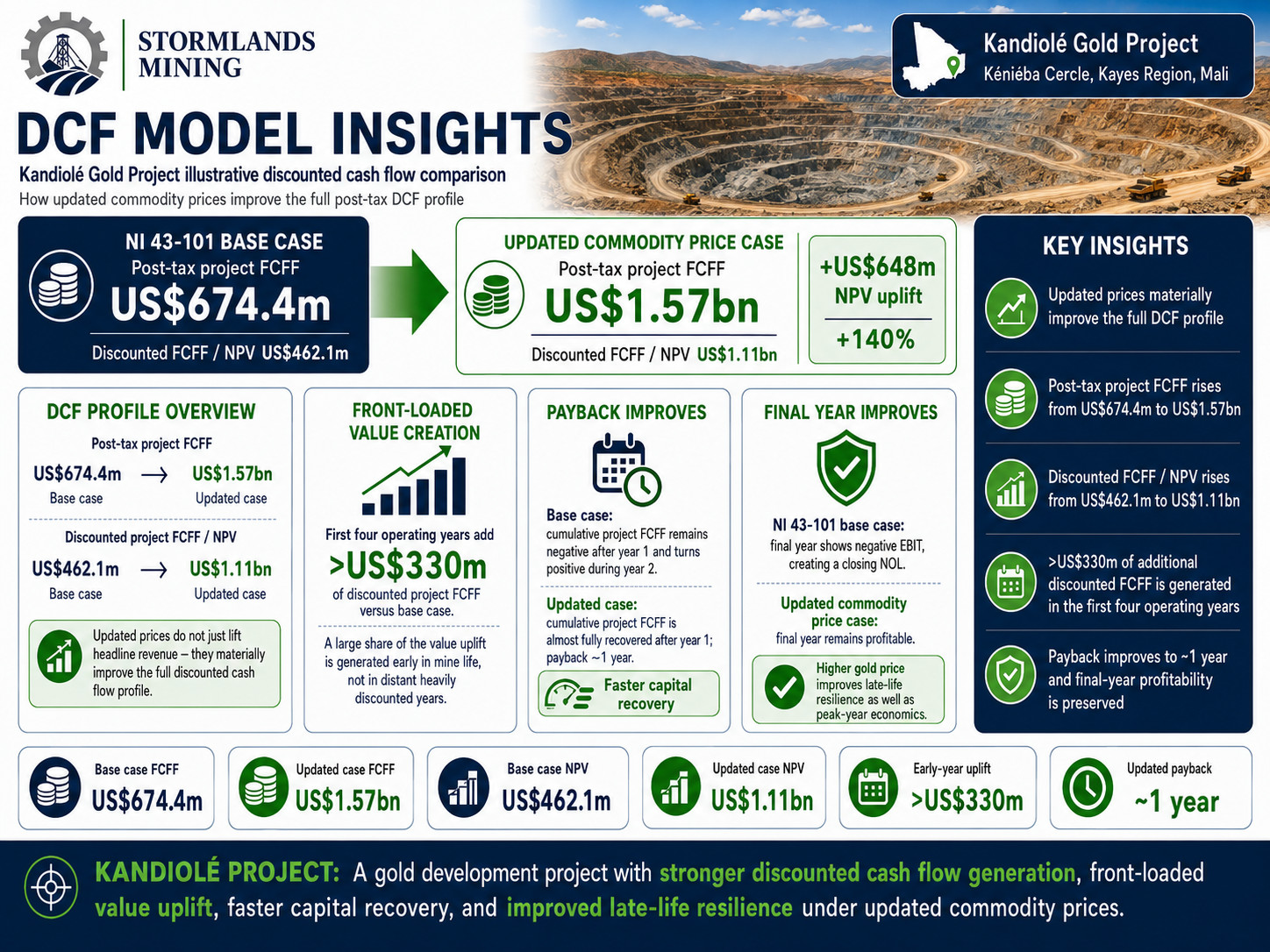

DCF Model Insights

The DCF comparison shows that the updated commodity price case does not merely increase headline revenue. It materially improves the full discounted cash flow profile.

In the NI 43-101 base case, the project generates post-tax project free cash flow of approximately US$674.4 million. Under the updated commodity price case, post-tax project free cash flow increases to approximately US$1.57 billion.

Discounted project free cash flow, which drives NPV, increases from approximately US$462.1 million to approximately US$1.11 billion.

The uplift is not limited to late-life cash flows. A large portion of the increase is generated early in the mine life. In the first four operating years, the updated commodity price case adds more than US$330 million of discounted project free cash flow compared with the NI 43-101 base case.

This is important because it shows that the updated price case is not dependent on distant, heavily discounted cash flows. The value impact is front-loaded and improves capital recovery.

In the NI 43-101 base case, cumulative project free cash flow remains negative after the first operating year and turns positive during the second operating year. In the updated commodity price case, cumulative project free cash flow is almost fully recovered after the first operating year, with payback achieved at approximately one year.

The final operating year also improves. In the NI 43-101 base case, the final year shows negative EBIT, creating a closing net operating loss. In the updated commodity price case, the final year remains profitable, demonstrating that the higher gold price improves the resilience of late-life production as well as peak-year economics.

Value Drivers

The Kandiolé model shows a clear hierarchy of value drivers.

- Gold price

Gold price is the dominant driver of project value. In both the NI 43-101 base case and the updated commodity price case, the price factor and gold price factor have the largest impact on NPV.

In the NI 43-101 base case sensitivity analysis, the NPV range for gold price movement is approximately US$348 million to US$576 million. In the updated commodity price case, the equivalent range is approximately US$933 million to US$1.29 billion.

The updated price case therefore has a much wider absolute value range. A 10% movement in gold price has a much larger dollar impact when the project is being valued from a higher gold price base.

- Operating cost

Operating cost is the second most important valuation driver.

In the NI 43-101 base case, the operating cost sensitivity range is approximately US$416 million to US$508 million. In the updated commodity price case, the operating cost sensitivity range is approximately US$1.06 billion to US$1.16 billion.

The absolute operating cost sensitivity is broadly similar in both cases because the cost base is unchanged. However, operating cost risk becomes less significant relative to the larger NPV in the updated price case.

In other words, higher gold prices increase the project’s resilience to operating cost inflation.

- Discount rate

Discount rate has a more limited impact than gold price or operating cost.

In the NI 43-101 base case, the discount rate sensitivity range is approximately US$445 million to US$479 million. In the updated commodity price case, the range is approximately US$1.07 billion to US$1.15 billion.

This reflects the project’s strong early cash flow profile. A meaningful portion of value is generated in the early years, reducing the project’s relative exposure to discount rate changes.

- Capital cost

Capital cost is the smallest of the main value drivers tested.

In the NI 43-101 base case, the capital cost sensitivity range is approximately US$446 million to US$478 million. In the updated commodity price case, the range is approximately US$1.09 billion to US$1.13 billion.

This does not mean capital discipline is unimportant. It means that, in this model, changes in gold price and operating costs have a much greater impact on valuation than equivalent percentage changes in capital cost.

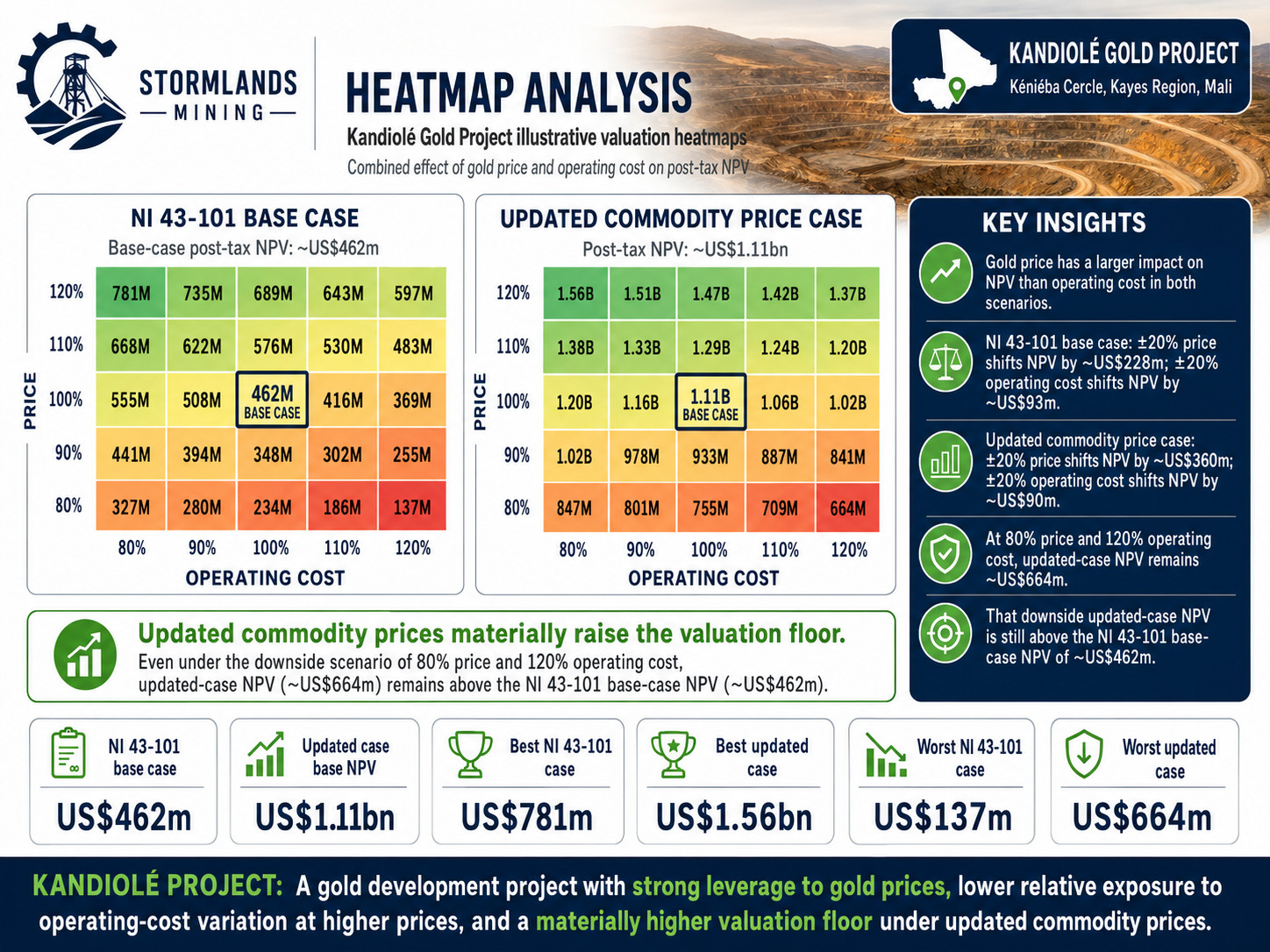

Heatmap Analysis

The price and operating cost heatmaps show the combined effect of commodity price movement and operating cost variation.

In the NI 43-101 base model, the base case NPV is approximately US$462 million. At 120% price and 80% operating cost, NPV increases to approximately US$781 million. At 80% price and 120% operating cost, NPV falls to approximately US$137 million.

In the updated commodity price case, the base case NPV is approximately US$1.11 billion. At 120% price and 80% operating cost, NPV increases to approximately US$1.56 billion. At 80% price and 120% operating cost, NPV remains approximately US$664 million.

This is one of the strongest findings in the case study. Even under the downside heatmap scenario of lower gold price and higher operating cost, the updated commodity price case remains above the NI 43-101 base base case.

This demonstrates that the updated price environment materially raises the valuation floor for the project.

The heatmap also shows that gold price has a larger effect than operating cost in both scenarios. In the NI 43-101 base case, a 20% movement in gold price changes NPV by approximately US$228 million, while a 20% movement in operating cost changes NPV by approximately US$93 million. In the updated commodity price case, a 20% movement in gold price changes NPV by approximately US$360 million, while a 20% movement in operating cost changes NPV by approximately US$90 million.

This means the project becomes even more price-leveraged, and relatively less exposed to operating cost variation, as the gold price increases.

About Stormlands

Stormlands Mining is an AI-first valuation and analytics platform for mining assets and critical minerals. The platform enables users turn technical disclosures into interactive valuation models in minutes, rather than days or weeks. The valuation models are accessible over multiple platforms to all levels users, enabling the user to interact directly with the data to facilitate scenario-planning.

The platform enables users to build discounted cash flow models at scale, test commodity price, capex, opex, tax, royalty rates, discount-rates and production scenarios, and compare opportunities and scenarios.

Stormlands uses its own technology to build the Stormlands Library: a global repository of mining asset valuation models. It has moved beyond a tool for analysts building individual models and is developing a data layer for the mining industry: a structured source of valuation models and illustrative scenarios. This creates a new way for investors, corporates, professional advisers, financial-market users and public-policy stakeholders to screen assets, benchmark projects and understand the key drivers of mining asset economics.

Commercial Interpretation

Kandiolé is a strong example of why mining economic models should not remain static after a technical report is published.

The NI 43-101 base model already shows robust economics. At a gold price of US$3,100/oz, Kandiolé generates a post-tax NPV of approximately US$462 million, an IRR of 48.9% and a short payback period.

However, when the same model is updated to a gold price of US$4,877.40/oz, the valuation changes materially. Project NPV increases to approximately US$1.11 billion, IRR increases to 97.0%, and payback improves to approximately 1 year.

The updated case does not rely on a revised mine plan, increased production, higher grade or reduced costs. It is the same economic model updated for commodity price.

For investors, this provides a clearer view of current valuation and upside exposure.

For mining companies, it provides a structured way to communicate how market conditions affect project economics.

For advisers and analysts, it provides a repeatable workflow for comparing projects, testing assumptions and identifying the assumptions that matter most.

For governments and other stakeholders, it helps show how changes in commodity prices affect not only shareholder returns but also royalties and tax revenues.

Why this matters

Technical reports provide the foundation for understanding a mining project. However, they are usually static documents. Commodity prices, exchange rates, capital markets, operating costs and investor expectations can move quickly after publication.

The Kandiolé case study demonstrates the value of converting technical disclosure into a live model.

A static report can tell users what the project looked like under a defined set of assumptions. A dynamic model can show how the project behaves as those assumptions change.

For Kandiolé, updating the gold price alone increases life-of-mine revenue by approximately US$1.47 billion, more than doubles EBITDA, increases post-tax NPV by approximately US$648 million, and materially increases projected government revenues.

This is precisely the type of analysis that is difficult to perform quickly using static PDF disclosure alone.

Stormlands Conclusion

The Kandiolé case study demonstrates the value of turning NI 43-101 technical disclosure into a dynamic, scenario-ready valuation model.

Using the technical report base case assumptions, Stormlands created a base case valuation of approximately US$462.1 million NPV. Updating the model to current commodity price assumptions increased project NPV to approximately US$1.11 billion.

That uplift of approximately US$648 million illustrates how sensitive gold project valuations can be to commodity price assumptions, and why static technical report numbers can quickly become outdated in fast-moving markets.

The analysis also shows that Kandiolé is primarily driven by gold price, with operating cost as the second most important value driver. Capital cost and discount rate are less influential in the model, reflecting the project’s strong early cash flow profile and rapid payback.

Stormlands enables users to extract data from technical reports, build valuation models, update commodity prices, test sensitivities, evaluate downside cases and compare projects in a consistent and transparent way.

The Kandiolé model is part of the Stormlands Mining Library, a growing repository of dynamic mining valuation models built from public technical reports and company disclosures.

About Stormlands

Stormlands Mining is an AI-first valuation and analytics platform for mining assets and critical minerals.

The platform enables users to turn technical disclosures into interactive valuation models in minutes, rather than days or weeks.

Stormlands enables users to build discounted cash flow models at scale, test commodity price, capex, opex, tax, royalty rate, discount-rate and production scenarios, and compare opportunities and scenarios.

Stormlands is using the platform to build the Stormlands Library: a global repository of mining asset valuation models. The Library provides a structured source of valuation models and illustrative scenarios, enabling users to screen assets, benchmark projects and understand the key drivers of mining asset economics.

Important Notice

This publication has been prepared by Stormlands Mining Ltd. for informational, educational and illustrative purposes only. It is based on publicly available information, including updated Mineral Resource Estimate and Preliminary Economic Assessment with an effective date of 4 December 2025 , together with independent modelling undertaken by Stormlands Mining.

Stormlands Mining has not been engaged by the project owner or its affiliates to prepare this analysis. This publication has not been reviewed, approved or endorsed by the project owner, its advisers, or any Qualified Person associated with the Project.

The analysis presented is not a Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, technical report, mineral resource estimate, mineral reserve estimate, valuation opinion, fairness opinion, investment research report, securities recommendation, offer to sell, solicitation to buy, or investment advice.

Stormlands Mining is not acting as a broker, dealer, investment adviser, corporate finance adviser, Qualified Person, or securities research provider in connection with this publication.

All model outputs are scenario-based and depend on the assumptions used, including commodity prices, exchange rates, discount rates, capital costs, operating costs, taxes, royalties, production schedules, payability, recoveries, treatment and refining charges, timing assumptions and other inputs. Actual results may differ materially from the scenarios presented. Commodity prices, costs, financing conditions, permitting timelines and project development outcomes are uncertain and subject to change.

Stormlands Mining does not represent or warrant that the information or model outputs are complete, accurate or suitable for any particular purpose. Readers should treat this publication as one source of information only and should conduct their own independent technical, financial, legal, tax and investment due diligence before making any decision.

Neither Stormlands Mining nor any of its directors, officers, employees or advisers accepts any liability for any loss arising from reliance on this publication or the information contained in it.